In This Article

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

Benjamin Graham

Remember when you bought a stock at its lowest low and sold it at its highest high?

Oh, right. You don’t remember because it never happened.

That’s because nobody can time the market perfectly. I can’t. You can’t. Warren Buffett can’t. If anyone tells you they can, they likely have some beachfront property in Arizona to sell you as well.

The funny thing is you don’t even have to try timing the market. If you have the patience and fortitude to stick with a simple plan, you can do the next best thing, which is to never overpay for stocks or never worry about waiting around for a bottom.

The key to this strategy is dollar-cost averaging. Instead of going all in on a stock in one fell swoop, dollar cost averaging allows you to buy a small amount of the stock over time. It’s more akin to playing a dozen hands of poker with small bets instead of pushing all your chips onto the table at one time.

What is Dollar Cost Averaging?

It’s really quite a simple strategy if you can keep your cool and ride out any storms. However, it does require a plan and the stomach to stick to it — especially if the markets continue to drop. That’s because the plan involves buying a fixed dollar amount of a particular stock, fund, or index on a regular schedule regardless of its price.

That is usually where most retail investors generally fail because, to a large extent, they have it all backward — they love buying the hype and selling the fear.

You have the power of patience.

Dollar-cost averaging does make sense even though it often involves overcoming those same fears as stocks “go on sale.” The reason is simple: Using dollar-cost averaging, more shares are purchased when prices are low, and fewer shares are bought when prices are high.

The result is that over time, the average cost of your shares will become smaller and smaller. Since dollar-cost averaging spreads out your stock purchases, it lessens the risk that you will buy them at the wrong time.

Instead, you arrive at an average price that typically reflects the true value of those shares.

Here’s how it works in practice…

How to Dollar Cost Average

You have $10,000 that you want to invest in a tried-and-true blue chip stock that looks attractive. Let’s say, for example, that it traded for $50 a share on the day you decided to pull the trigger.

Spending every penny of that $10,000 in one trade would carry a hefty risk along with it. If a bear market came rolling in, you would be at an immediate loss with nothing left to buy more shares. In short, you’d be stuck with 200 shares at $50.00 apiece. That is no way to safely grow your fortune.

You see, if you broke up that same purchase into four equal parts and scaled into your position during the downturn, your average price would be much lower.

Here’s what I mean…

Let’s say you broke up that $10,000 into four separate $2,500 purchases. Instead of buying them all at $50, you can break them into buys of $44, $51, $45, and $50. That way, you’d end up with 211 shares at $47.39 each. That’s the best of both worlds: more shares for less cost per share.

That puts you in a far greater position when the market finally turns around. Better yet, you wouldn’t have to guess exactly where the bottom was along the way. And when the market turned — as it always does — you would be there to reap the benefits.

When to Break the Rules

Some dollar cost averaging devotees will set a concrete buying schedule: “I’ll buy $100 worth of Home Depot (NYSE: HD) stock at the beginning of every month.” That is all well and good.

However, there are clear times when you can buy Home Depot stock at a much cheaper rate…

Like right now, for instance. With rising interest rates and inflation cutting into the business, you would be better off putting more of your capital into it instead of a random monthly contribution. You’d lower your cost per share over the long haul.

This is called “buying the dip,” and despite my warnings about timing the market, it can be useful for positions that you want to hold long term. That makes dollar cost averaging a nimble tool: you can tweak it to fit the current market without trying to time it exactly.

But you can play the game between the lines while building a lifetime portfolio.

In the end, trying to time the bottom is a fool’s errand. Trying to time the top is when investors get greedy and try to ride a stock “to the moon.”

Instead, you should be wading in one step at a time, using dollar-cost averaging as your guide — especially as the market heads downward. I’d venture that you should be buying more when we hit new lows.

You can automatically dollar cost average by purchasing a dividend reinvestment program. These DRIPs will take your dividend payments and invest them back into the stock, regardless of how high or low its trading. When one of my major DRIP stocks takes a beating, I load up on stocks in the DRIP, knowing that eventually, the company will snap back, and I’ll have filled up my coffers at the lowest possible price.

So, when you combine the efficiency of dollar-cost averaging with the “Rule of 72”, you unleash the power of a dividend investment portfolio.

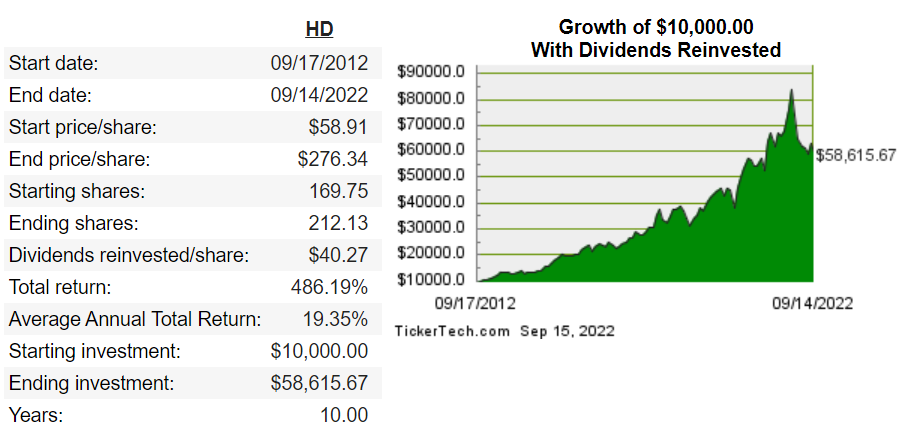

Take a look at that Home Depot stock over the past ten years, assuming that you put the $10,000 into it over some time and enrolled in the DRIP:

That’s why set-it-and-forget-it stocks almost always outperform the market when you buy them the right way. If you really think a stock – like Home Depot – will be around for the next few decades, it behooves you to slowly build your positions in good times and bad.

You can easily do this with index funds like the ProShares S&P 500 Aristocrats ETF (BATS: NOBL). They follow the market, so you don’t have to.

Otherwise, find a fit for your finances and your risk tolerance. If you can drop $100 or more on a single stock every month, do so. If you happen to be flush with cash when one of your favorite stocks goes on sale, have at it.

Don’t overdo it in either direction – you don’t want to be pulled apart by horses.

The one thing you should never do is sink or swim on one single stock. Wade into it. See how the water feels. Swim accordingly. Don’t sink.

Don’t be afraid of the word “average.” Your returns will be far from average if you stick to your guns and slowly allow your money to create itself.

Godspeed,

Jimmy Mengel

The Profit Sector