- The Energy Sector Going into 2023

- Coal, the Zombie Fuel

- Boatloads of Natural Gas

- American Oil’s Golden Years

- Wild Times, Wild Profits, Winding Down?

One thing. That’s all that matters in the energy sector.

So much change, so much going on. Analysts can equivocate as much as they want, and they certainly will.

But one and only one thing matters now – Extraction. That’s the reality in the energy sector in 2023.

What does that mean?

If you’re stuck in the old paradigm, it might seem like it’s pulling more from fracked wells, both oil and natural gas, and moving earth for coal.

Sure, that still matters, but no.

Instead, we’re talking about wealth extraction. Cash flows, shareholder returns, and arbitrage plays on what exists now.

The energy sector in 2023 is going to be about the payout. There's no way around it.

The Energy Sector Going into 2023

We’re looking at an energy sector in the twilight of an unprecedented surge in profits and share prices.

2023 is going to be compared to 2022, year-over-year and quarter-over-quarter, as is usual in the stock market. These standard metrics won’t look as impressive in comparison.

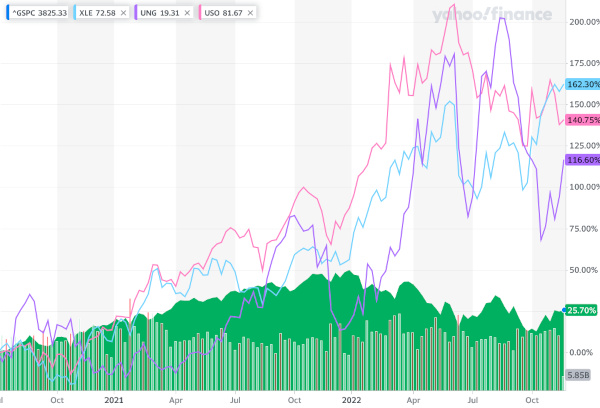

Just look at the two-year chart of the S&P 500 versus the Energy Select Sector SPDR Fund ETF (NYSE: XLE), United States Natural Gas Fund (NYSE: UNG), and United States Oil ETF (NYSE: USO).

These are incredible gains that will be hard to beat. Plus, with inflation and the risk of a recession, virtually no one anticipates anything similar going forward.

The World Bank, in a comprehensive October 2022 report, expects overall energy costs to drop 11% in 2023 after a 60% surge in 2022.

That still retains a 75% increase over the five-year overall average. Plus, it glosses over some key details.

Any energy company in a good position to pull in profits won’t try for a market share grab. That’d mean more debt at higher interest rates for capital expenditures. It’d add a burden to their ledgers.

Yet that doesn’t mean there isn’t a whole lot of potential left for investors to profit. Just the opposite, if anything. Companies that can rake in money in the short term will do it, and be seen as safe havens by investors.

Let’s break it down by fuel types. Plus, we can talk about how we can capitalize on them as we go.

Coal, the Zombie Fuel

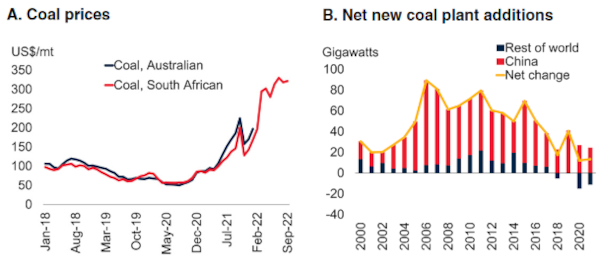

One of the biggest stories of 2022 was the resurgence of coal.

Old mines and power plants reactivated. Energy-starved Europe and priced-out developing countries returning to a dependable and common source of power.

Coal prices surged beyond anything anyone could anticipate, with a 5-year gain of about 350% and 120% in the last year.

The argument against coal is clear. Geopolitical issues in Europe and the stark reality of keeping power grids active in the vast “developing world” as other fuel prices spike created a short-term need.

Turn this around, though, and coal is exactly what was required in a time of desperation. It won’t be the last.

Any shock to the global system that pushes energy prices off ‘bargain bin’ levels may result in the same kind of reaction.

There certainly was money made. There may be more potential.

According to the World Bank report, Australian coal, in particular – conveniently close to the world’s largest markets in Asia – is expected to see price drops but stay over twice its five-year price average even as coal use increases in the region.

Buying into a shrinking market in the long term is hardly something we need to do. Plus, the reactionary stock market play is probably over.

Extremely large companies that produce thermal coal will have limited overall exposure to future price changes. Small companies in the sector are plagued by high debt burdens that will become crippling if prices drop.

As a result, we’re choosing not to mention any particular stocks for 2023 for thermal coal – the type used for power generation. The limited upside versus the steep downside isn’t even. We can find better investments elsewhere.

As a side note, metallurgical coal is an interesting – and critical – subsector, but we won’t delve into that today.

It is very fascinating how quickly a lot of nations reverted back to coal, though. It’s become a kind of zombie fuel, declared dead many times but always somehow showing some signs of life.

The lesson to learn is that the world economy needs baseline fuels. All the talk about moving away from dirty fossil fuels cannot change that, when push comes to shove, the global energy market quickly falls back upon cheap energy production.

Coal is still king in that regard.

Coal’s cousin – natural gas – was the heir apparent, but offers its own kind of cautionary tale.

We absolutely need to look at how it will evolve in 2023.

Boatloads of Natural Gas

The best way to start talking about natural gas in 2023 is to talk about Europe.

Take a look at this:

That’s the first of a pair of liquified natural gas terminals under construction in Wilhelmshaven, Germany. A second is being built in Brunsbuettel. Both are slated to become active around the start of the year after a nearly $7 billion investment.

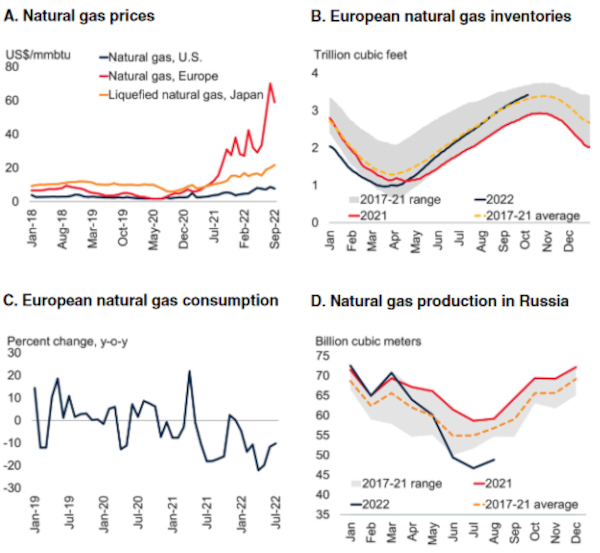

It’s just the start. The “floating storage and regasification units” are two of six slated to be active by 2024. Combined, they can theoretically import a third of Germany’s demand based on 2021 numbers – 90.5 billion cubic meters.

It’s a massive amount but in 2021, EU nations consumed just shy of 400 billion cubic meters and imported about 83% of it. The need for more imports, and the capacity for more over time from overseas, is mind-boggling.

The EU’s commitment to wean itself off Russian gas pipeline supplies is questionable, in my opinion. Europe will quietly pay as long as fuel is for sale, and it will be as long as Russia wants money, but maybe not quite enough.

However, I have no doubt that there is a lot of room for reducing that dependence, even if it costs a small fortune in upfront building costs. Thus, there is room to find new sources at any lower cost, even if there are massive upfront costs, like building LNG regasification terminals.

Few natural gas producers are better positioned – geographically and politically than those in the USA.

While the World Bank report suggests domestic USA prices will stay twice as high as the five-year average – coming off near historic lows – European natural gas prices are already four times higher.

Expanded import capacity from LNG terminals will provide capacity to drive down costs in Europe. Even then, LNG prices in Asia are a floor, with two-to-one differences still offering an arbitrage play.

2023 natural gas prices will be purely based on two factors – the differences in these prices and any effect from a recession.

A stock to watch in 2023 is one we’ve watched for years – Cheniere Energy, Inc. (NYSE: LNG).

No other domestic natural gas play has as much capacity to export natural gas. However, it is in a negative earnings-per-share scenario as it expands its operations.

Other major players in the market are Shell Plc (NYSE: SHEL) and TotalEnergies SE (NYSE: TTE).

They are much larger – with market capitalizations of $204 billion and $151 billion, respectively – and far more lucrative dividends – 3.66% and 4.66%, respectively – but have much more diversified operations.

With Cheniere Energy, Inc. (NYSE: LNG) positioned in the USA for an unparalleled arbitrage play and with insatiable demand in Europe and Asia, it’s stock to watch as long as global LNG demand persists.

There are other options for ways of extracting wealth from natural gas plays, namely pipelines, and MLPs. After all, natural gas is one of two parts of the USA’s renewed role as an energy exporter.

Oil production outside of OPEC has become a big issue. And the most lucrative trends and stocks in the oil game may be involved.

American Oil’s Golden Years

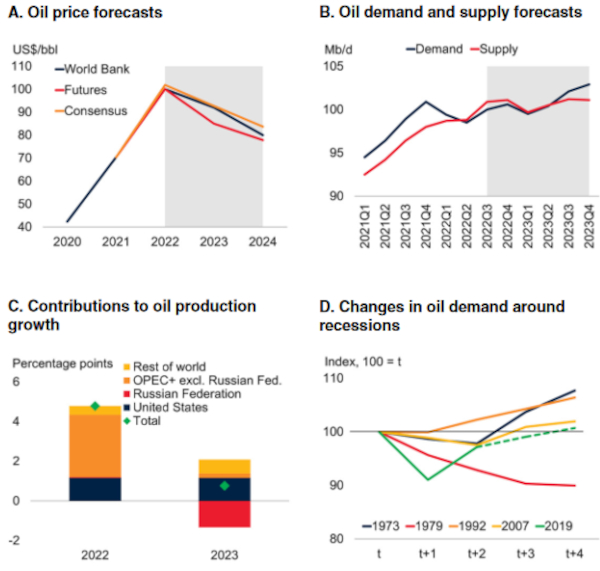

Oil prices have surged in recent years, alongside a growing gap between supply versus demand, yet we will still probably see a drop in price.

The World Bank report predicts a modest drop from $92 a barrel in 2023 to $80 in 2024 in the Brent oil benchmark prices.

There is still plenty of money to be made.

With oil prices flat, at best, and falling, most likely, now isn’t the time to chase after new production.

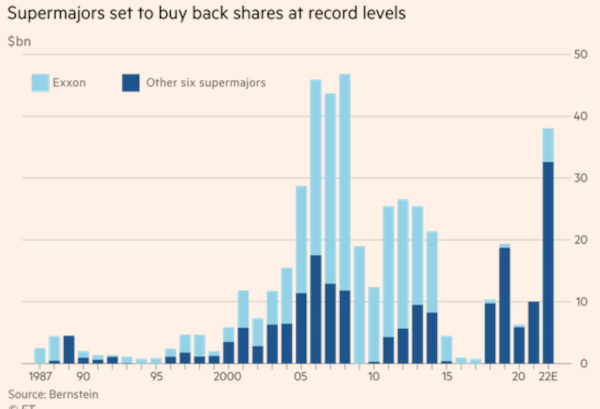

Instead, we’ll see a continuation of a multi-year trend. Oil companies are going to return money to shareholders via share buybacks and dividends.

Major oil companies reinvested in themselves at record levels in 2022.

It isn’t even worth listing all the companies that increased their dividend payments in 2022. It’s an oil company worth mentioning.

As an example, ConocoPhillips paid out $1.40 per share on October 14th. That special dividend is on top of the regular one at $0.46. That’s a full year’s payout in one quarter.

These were windfall payouts on top of the share buybacks that return value by reducing the number of shares outstanding.

Similar payouts may occur going forward, but they are not guaranteed.

They make one thing clear, though – oil companies want to keep their investors by returning money to them. Just looking at dividend yields for some of the largest energy companies out there, as this is written…

- TotalEnergies SE (NYSE:TTE) pays 4.66%

- Suncor Energy, Inc. (NYSE:SU) pays 4.32%

- BP plc (NYSE: BP) pays 4.04%

- Shell plc (NYSE: SHEL) pays 3.66%

- Exxon Mobil Corp (NYSE: XOM) pays 3.25%

- Chevron Corp (NYSE: CVX) pays 3.1%

Then there are the pipeline companies which are designed to give consistent payouts to shareholders since they are structured as MLPs, or “master limited partnerships”. Again these are some of the largest, and yields are from when this was written…

- Energy Transfer (NYSE: ET) pays 8.49%

- Enterprise Products Partners (NYSE: EPD) pays 7.69%

- Enbridge (NTSE: ENB) pays 6.32%

- Kinder Morgan (NYSE:KMI) pays 5.93%

- ONEOK, Inc (NYSE: OKE) pays 5.72%

- TC Energy (NYSE: TRP) pays 5.5%

While there are plenty of other oil companies out there, going into 2023, we’re looking to stick to the large ones with economies of scale working in their favor.

Sure, growth would be nice, and their scale works in their favor in a high-yield environment, but we’re looking for solid free cash flow. The kind that comes back to us without breaking the bank.

For the big oil companies, there isn’t a whole lot of difference, but Chevron Corp (NYSE: CVX) is the most aggressive with share buybacks going forward, even as it offers the lowest dividend yield. With how variable inflation and market outlooks are, it can quietly shy away from it and free up cash, which makes it stand out to me.

As for MLPs, the high-interest rate environment makes matters tough, but Kinder Morgan (NYSE: KMI) has a particularly strong balance sheet compared to its peers. It’s probably the go-to MLP investment overall.

ONEOK, Inc (NYSE: OKE) is coming off major expansions in recent years but is in a good spot to capitalize on capacity and free cash flow potential. This is a company I’d actually want to hear little news about – a couple of quarters of shoring up its volume and capacity in small ways and committing to an improved balance sheet may position it as an industry standout.

Wild Times, Wild Profits, Winding Down?

If there is one truth about investors, it's far easier to whip them into a frenzy than to wind them down.

The last several years have seen a dramatic reversal of fortunes for energy sector investors. Massive gains across the board, special dividends returning windfalls, the list goes on and on.

It has been practically raining money. Wild times and wild profits.

Is that party at an end? Maybe for the kind of stock gains that draw in “fair weather fans”, so to speak. But not for investors that want to capitalize on some of the consistent gains the best in the sector will return.

In 2023, I'm skipping coal entirely, sticking to Cheniere Energy, Inc. (NYSE: LNG) as a natural gas play because of its export capacity, expecting Chevron Corp (NYSE: CVX) to outperform in overall return to shareholders through a mix of dividends and buybacks, and thinking Kinder Morgan (NYSE: KMI) will pay out as a higher yielding MLP investment without much risk of outsized share value drops.

Fair warning, all of this is relative and should be compared to their peers. Who knows where the economy and markets go from here. All signs point to the kind of returns that will beat the broader stock market in a dependable way. The kind of returns where we won't need to watch the news like hawks. Where we won't lose sleep, or hair, or sanity.

That sounds pretty good these days. I'm trying to keep all three.

Take care,

Adam English

The Profit Sector