When you think about the all-time greatest bank robbers, George Leonidas Leslie may not be the first that comes to mind…

John Dillinger, Billy the Kid, and Bonnie and Clyde all made more headlines and have become American folk heroes.

That’s because Leslie wasn’t a gun-wielding outlaw, he was a well-to-do New York architect that relied on his wit instead of a pistol. Leslie focused his talents on studying the inner workings of locks, drafting up entire blueprints of the banks he had his eyes on, and even inventing his own mechanical safe-breaking devices.

Leslie even created scale models of the banks so that he didn’t leave anything to chance.

He was methodical in his approach, and it paid off big time. An astounding 80% of all bank robberies from 1869 to 1878 are attributed to Leslie. All told, his heists brought in $7 million in ill-gotten gains (worth $200 million today).

His final heist is still considered the largest in history. Leslie and his gang spent three years casing the Manhattan Savings Institution and planned the robbery for October of 1878. The gang pulled in $80 million in today’s dollars in one fell swoop.

When all was said and done, Leslie was dubbed “The King of Bank Robbers” by the NYPD.

But like almost all of history's bank robbers, things did not end well for George Leonidas Leslie. He disappeared shortly after his greatest heist and was found a month later, dead under a bush in Yonkers with two gunshots to the back of his head.

His murder was never solved…

A High Tech Bank Robbery

If Leslie had been robbing banks this month, he would probably be rather disappointed when he cracked the safe and realized that there was a lot less money in there…

Earlier this month, after the collapse of Silicon Valley Bank scared the bejeezus out of the entire investment world, the four biggest U.S. banks lost $52 billion in a day.

- JPMorgan lost about $22 billion in market value

- Bank of America lost roughly $16 billion

- Wells Fargo's market capitalization dropped $10 billion

- Citigroup was down $4 billion

That’s one bad day for banking. I’m sure the banks would have preferred an old-fashioned bank heist to the bloodbath that happened to their share prices. All told, the banking industry has more than $600 billion in unrealized losses on its securities holdings, according to the FDIC.

Trust Financial, Charles Schwab, JPMorgan, and Capital One Financial each have more than $10 billion in unrealized losses.

So with all of the uncertainty, why would anyone want to buy a bank stock right now?

Because it’s just the right time. As legendary banker Baron Nathan Rothchild famously said, “Buy when there is blood in the streets.”

Right now, there is still blood in the streets, but the Fed's actions seem to have started cleaning it up, leaving us with a chance at some great investments.

All Banks Are Not Created Equal

After the collapse of SVB, the Fed swooped in to arrange a bailout for the worst suffering banks. Treasury Secretary Janet Yellen has also announced the federal government could step in to protect depositors at additional banks if needed. On March 12, the Treasury, Federal Reserve, and FDIC issued a statement saying that the Fed would “make available additional funding to eligible depositary institutions to help assure banks have the ability to meet the needs of all of their depositors.”

It was welcome news to the banking industry and seems to have steadied further declines.

The bank crisis – and the Feds intervention – appears to have been just what the market needed. Instead of focusing solely on inflation, the Fed was able to stabilize the market with its emergency actions, and investors are piling back into stocks.

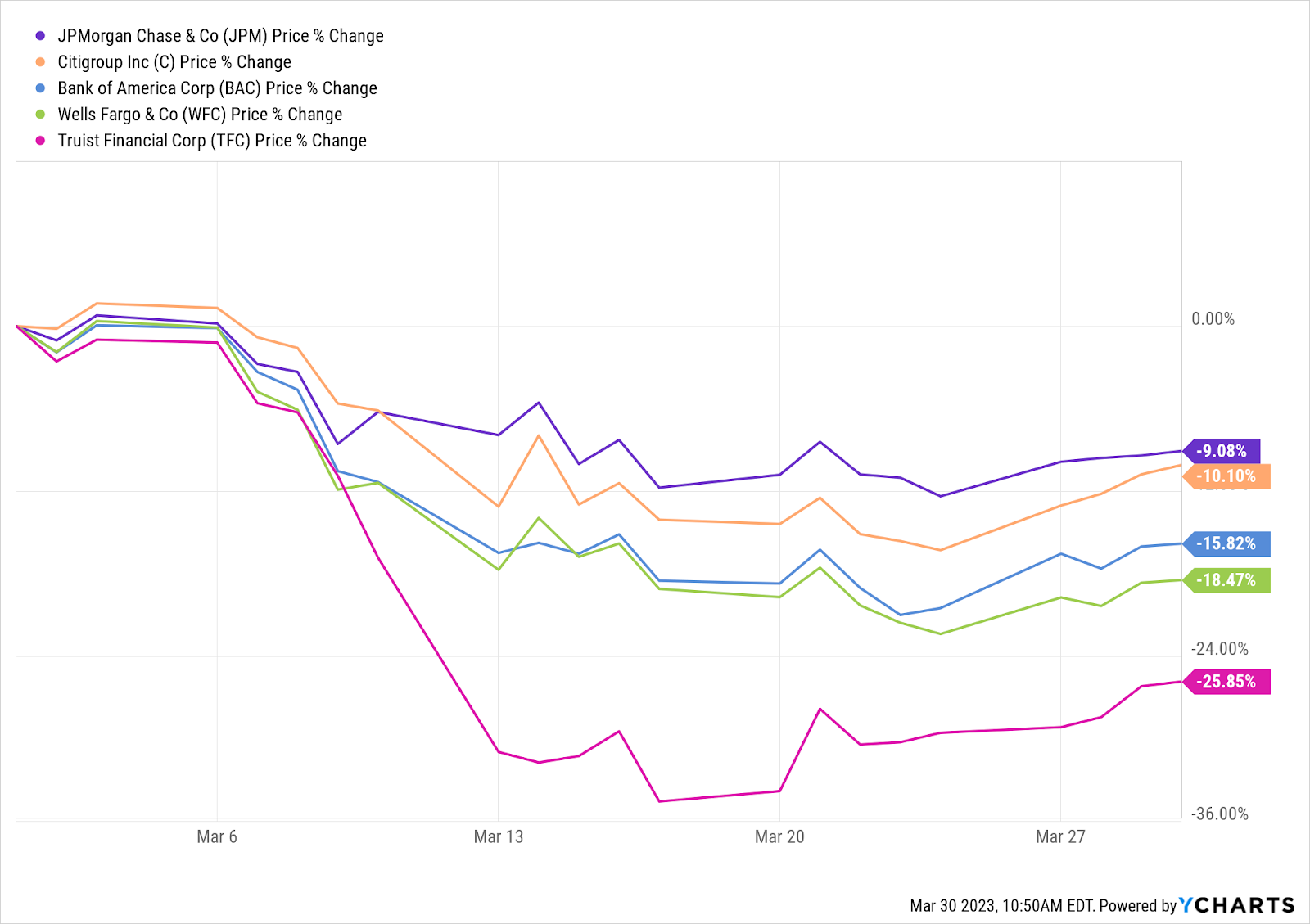

But the biggest banks have all experienced a haircut:

I’ve included the smaller regional bank Truist Financial (NYSE: TFC) in the above chart because I believe that is the best value right now.

Truist Financial (NYSE: TFC)

Truist Financial Corporation is an American bank holding company that operates 2,781 branches in 15 states. It is number 10 on the list of largest banks in the United States, with $555 billion in assets. Their insurance holding division is the seventh largest insurance broker in the world, with $2.27 billion in annual revenue.

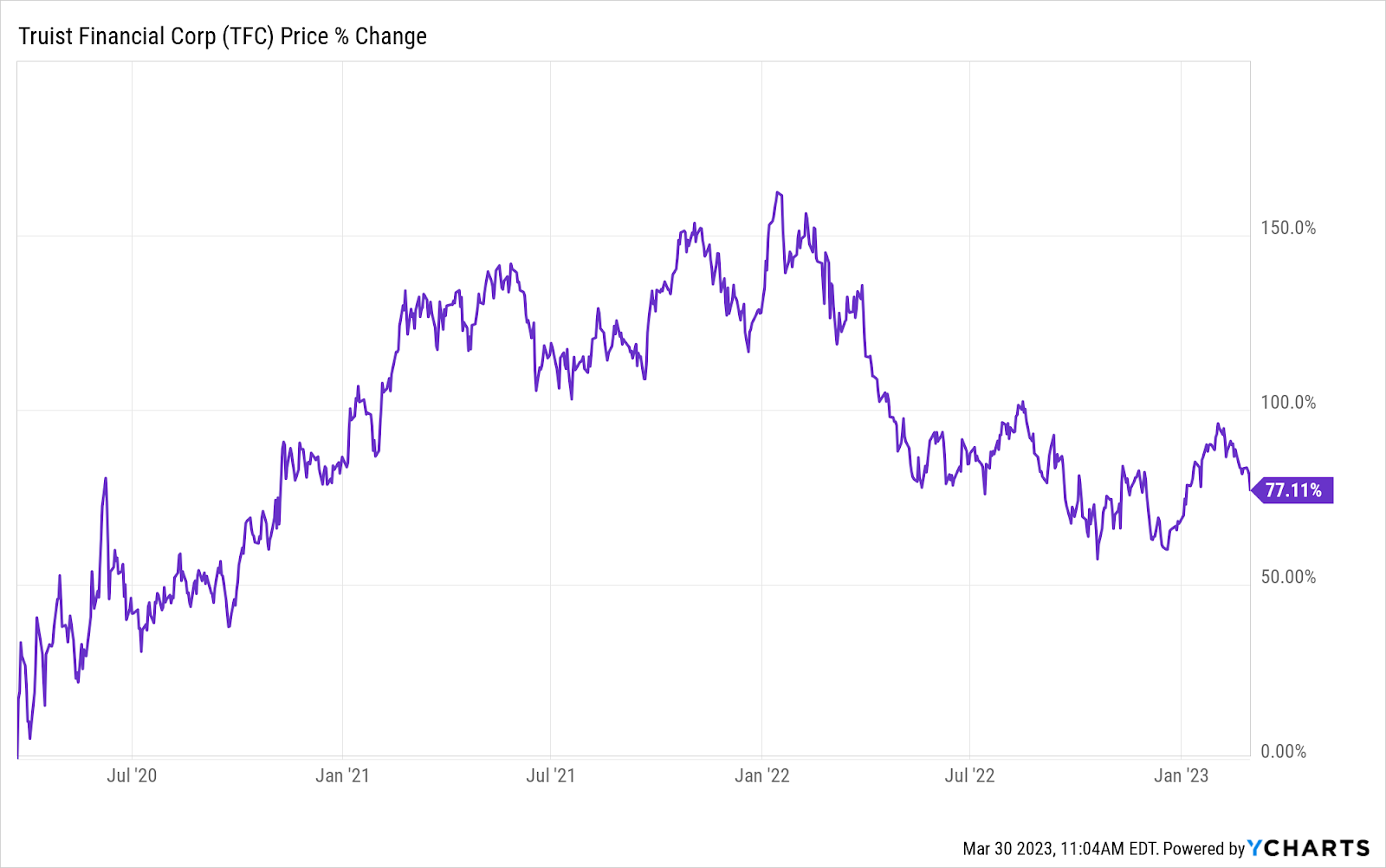

It’s not a household name like Bank of America or JP Morgan, but it has quietly delivered in the years since the 2019 merger of BB&T and SunTrust Banks. The company was up over 70% until the banking crisis earlier this month.

It appears to have the highest upside right now, as shares have dropped over 25% since the SVB debacle. But if you look at Truist, you’ll see that they have been punished by an overall fear in the sector, not because they are exposed to risky bets that took banks like SVB down.

While even heavyweights like Bank of America have nearly half of their equity impaired by bad loans, Trust only has 16.56%. The company is far less exposed than its peers.

Citi analyst Keith Horowitz has picked up on this and has called Truist “an apples and oranges comparison” to other afflicted banks.

In a note to clients, Horowitz predicted that Truist Financial shares can jump over 50% after their recent drop, citing that investors are wrong about the deposit outlook at Truist.

“The TFC bear case is all about high HTM [held-to-maturity] losses relative to equity, and we believe this thesis is flawed. Our view is that the deposit outlook is fine, meaning that securities can be held to maturity at par without realizing losses,” Horowitz said in the letter.

“Given the recent price action, we view this as an attractive entry point and are upgrading TFC to Buy.”

Horowitz set a $52 price target that looks incredibly appealing, considering that today the company is trading around $34. Add to that a safe, high-yield dividend of 6.4%.

Compare that with failures like First Republic Bank (NYSE: FRC), which just suspended its dividend entirely.

If you’re looking for a blood-in-the-streets bank play today, Truist looks like the cleanest shirt in the laundry. I would recommend buying on the weakness and enjoying that increased dividend yield.

Time will tell if we do end up going into a recession or if we see any other weak banks fail. I believe that the sector has stabilized for now, and you’ll be buying Truist at a significant discount.

Truist will report first-quarter 2023 financial results before the market opens If I’m correct, the company will post solid financials – especially in a fear-based bank environment – and that share price will rise considerably.

If you’re interested, investors can access a live audio webcast of the earnings call Thursday, April 20th, and view the news release and presentation materials at ir.truist.com.

At these prices, you may be able to pull off an impressive bank heist of your own.

Godspeed,

Jimmy Mengel

The Profit Sector

Follow me on Twitter @mengeled