The “Arsenal of Democracy” is for Sale, Payment Deferred

The Big Names In the Defense Sector

The Smaller, More Interesting Companies

Years of Spending and Investor Potential to Come

A year into the war in Ukraine and we’re still ignoring the obvious lesson learned over 80 years ago.

It’s one the USA has managed to handle so far, in short bursts, but a year on in a European war of attrition, we’d do best to look back.

Call them the “three B’s” – wars are won with bodies, bullets, and bombs.

[Former Goldman Sachs Vice President Calls This Defense Stock “AMERICA'S #1 RETIREMENT STOCK”.]

It invokes an old quote, one we should fear if just for what came next.

“We must be the great arsenal of democracy. For us, this is an emergency as serious as war itself. We must apply ourselves to our task with the same resolution, the same sense of urgency, the same spirit of patriotism and sacrifice, as we would show were we at war.”

It comes from one of President Franklin Delano Roosevelt’s “fireside chats.”

I will not dive into the politics or minutiae of the Ukraine war. You can find as much of that as you want elsewhere.

Instead, I want to talk about this kind of proxy warfare. It demands a lot more from us than we care to realize, and it will drive more spending than anyone – especially politicians – care to admit.

The FDR quote from what’s now known as the “Arsenal of Democracy” speech from December 29, 1940, was a declaration of proxy war.

The “Arsenal of Democracy” is for Sale, Payment Deferred

We’ve been through many wars since – Korea, Vietnam, Iraq, Afghanistan, those things down in South America we ignore, Syria, etc. Those are just the ones with direct involvement by the US military; others did not come with boots on the ground.

World War II taught us that US involvement could be far more – war by proxy, starting with material support.

Back at the end of 1940, when FDR uttered the words above via radio and nearly a year before the attack on Pearl Harbor, the USA had already started feeding Europe and Russia supplies.

Within a couple of months of being dragged into the war, a law written in response to World War I had already been circumvented by the Lend-Lease Program.

For a while, US-based companies had to take payment before delivering armaments. That isn’t the case if we expect token payments and that the armaments be returned in kind – never really an option, as you can imagine – at some undefined point in the future.

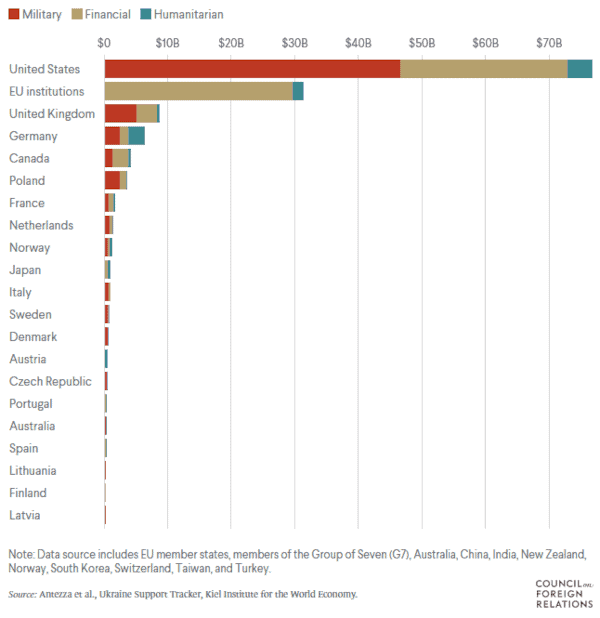

Here we are now. The USA and some EU countries are “lending” everything from bullets and bombs to drones and missiles to Ukraine.

We see nominal price tags in headlines, but no binding terms are involved with the aid provided.

We are at war regarding support yet again, yet we have not added the true cost to our balance sheets.

This is creating a deficit for stockpiles, supply agreements, and, ultimately, defense spending.

It’s carving out a special segment of our economy, on top of the fact that the USA was the top provider of weapons worldwide beforehand.

Defense stocks are uniquely positioned to see increased spending regardless of inflation or politics. It’s already started, the actual cost is vastly underestimated, and it’s far from a peak.

The Big Names In the Defense Sector

Defense spending is, for better or worse, as much of a political concern as anything else.

Speaking of presidential speeches, Dwight D. Eisenhower’s farewell speech in 1961 and its warning about the “military-industrial complex” rings true.

The big names in defense stocks will always do well. Think Boeing Co. (NYSE: BA), Lockheed Martin Corp. (NYSE: LMT), Raytheon Technologies Corp. (NYSE: RTX), and General Dynamics Corp. (NYSE: GD).

These companies aren’t immune to market sentiment, but they will exist in some form. They are constantly fed contracts – sometimes secondary to a primary contractor – as a contingency for Congressionally approved appropriation bills and will exist in some form going forward.

More niche stocks like shipbuilder Huntington Ingalls Industries Inc. (NYSE: HII) are equally embedded and protected, though they are much smaller by market capitalization.

All of these are good stocks to own, but consider how a program like the F-35 airplane – led by Lockheed Martin – was only finalized when it was guaranteed by law if other companies were involved.

In total, F-35 parts are produced in the 48 states in the US, along with seven partner nations as well as six FMS buyers. Something like 1,700 companies supply parts.

The big names are as much geopolitical conglomerates as they are US corporations. Perhaps that’s for the best, but it muddies the waters and makes headline procurement numbers misleading.

Regardless, they are too big to fail. They may not thrive, but they will always have work, delegate work, or find good terms for mergers if they fall out of favor.

As an investor, I’d almost consider these akin to ETFs with their own fiefdoms. They have their own proprietary blend of military and civilian revenue sources, and that blend may rise and fall, but they aren’t going anywhere.

In an environment where US and EU spending needs to rise regardless of cost – and has been – they are pretty insulated from volatility and act as barometers of overall activity and demand.

The Smaller, More Interesting Companies

One of the most interesting aspects of the war in Ukraine is the lack of air supremacy via traditional airplanes, the key feature of large-scale warfare in the last couple of decades.

We don’t hear about the kind of aerial bombardment we’re used to in asymmetrical conflicts – from the recent wars in the Middle East and Afghanistan in particular – in modern warfare.

Instead, we hear about artillery and ground-to-ground missiles. We hear about drones for target acquisition and cheap “suicide” missions via remote control.

Regardless, a constant struggle is in play, and it stays in limbo a year on, with little commitment from either side for increasing cost in dollars over lives.

There is a reason. It’s a matter of efficiency. Many advantages that may be gained no longer require dollars or bodies as they used to, and in a war of attrition, it could be crippling to deplete far more expensive resources. Plus targeting data and electronic warfare are on a whole new level.

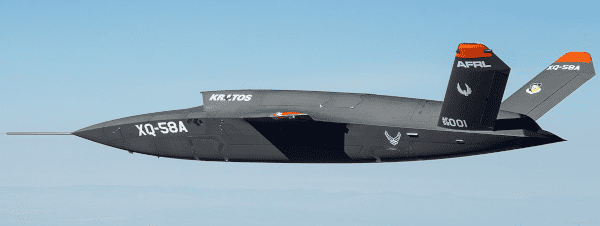

Kratos Defense & Security Solutions Inc. (NASDAQ: KTOS)

That’s where a company like Kratos Defense & Security Solutions Inc. (NASDAQ: KTOS) has an advantage.

Kratos is a company that, as it describes itself, specializes in unmanned systems, satellite communications, cybersecurity/warfare, microwave electronics, missile defense, hypersonic systems, training, and combat systems.

In other words, it’s a drone, satellite, and electronic warfare specialist. Everything that is necessary right now.

The company was founded in 1994 as Wireless Facilities Incorporated as a telecom infrastructure venture but shifted towards a defense company before long.

Acquisitions that supported a more specialized business model led to its current name and structure in 2007. Since then, its work has culminated in the XQ-58 Valkyrie unmanned aerial vehicle (UAV) and many US Department of Defense (DoD) projects, including land, ship, and aerial-based direct energy weapons – think lasers but not necessarily the kind that melts things.

Of particular note is the XQ-58 Valkyrie, specifically developed to act as a “loyal wingman” for the DOD’s highly integrated data systems in the F-35 and existing plane upgrade plans.

This is a customized pitch to the US and EU governments that use advanced warplanes they dare not lose. They can be commanded from afar, like anything else, but can also be controlled in real-time up close.

While Kratos is a leader in developing technology custom-tailored for a mission these countries claim as a priority, the problem is it is not pulling in revenue to support long-term revenue growth.

In other words, it is still operating on a wink and a nod from the government at a reasonable but constant negative earnings rate.

However, it is pulling in more and more revenue, and the divergence between stock price and revenues is interesting to track.

For the fourth quarter of 2022, Kratos clocked in as a $1.6 billion company by market capitalization, reported revenues of $249.3 million, an operating income of $4.1 million, a net loss of $8.3 million, an adjusted EBITDA of $19.2 million, and a consolidated book to bill ratio of 1.2 to 1.0.

This is a company that the US government will continue to invest in. However, there is no guarantee of net positive revenue for now. Or that the government wouldn’t play matchmaker for a larger company as an acquisition.

Without any new long-term contract announcements, it needs an influx of money investors won’t offer in a tech-adverse market, and the DoD won’t award outside of its arcane, multi-year grant system. That may be a fantastic opportunity, but it comes with risk.

Consider it a tech growth play, with an increasing demand for its products, including the potential for DoD approval of overseas sales, politically charged, of course, going forward.

Northrop Grumman Corp. (NYSE: NOC)

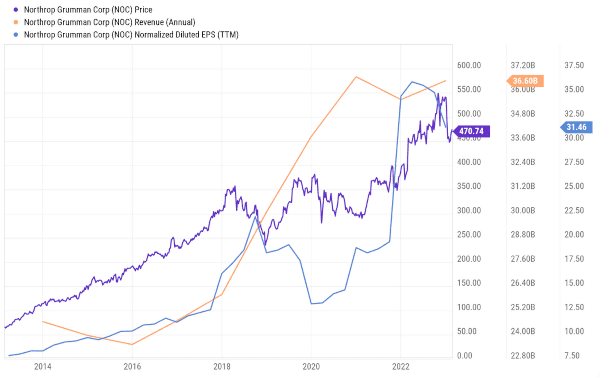

Another interesting play is Northrop Grumman Corp. (NYSE: NOC). It’s an old name in the defense sector that has fallen far behind market leaders like Boeing, Lockheed Martin, and the EU-based, subsidy-supported conglomerates.

However, the smaller size and its niche market expertise can and will work to its advantage.

For example, at the end of January 2023, Northrop Grumman Systems Corp. and Global Military Products Inc. (privately held) secured a $522 million order between them for 155 mm artillery shells and missiles amid worries that Ukraine was fast depleting the stockpiles of armaments from the United States and other allies.

Northrop Grumman is a $72 billion company by market capitalization, but it has been searching for new revenue sources. This contract is a strong indicator that it has renewed potential no other companies will fight (read as retooling existing manufacturing lines) going forward.

It’s also profitable, with a 31 earnings-per-share ratio and a 1.45% dividend yield. These aren’t great numbers, but they’re something. The company is not suffering, but it stumbled early in 2023 and that may make for an advantageous entry point for the stock.

What will be more interesting is an expansion of procurement on top of the contract mentioned above. These are specialized products not produced elsewhere by others, they’re being depleted at an alarming rate, and their importance is newly apparent.

That is recently being appreciated by Congress and its appropriations. Here are some select quotes from the New York Times:

- “Spending on procurement would rise sharply next year, including a 55 percent jump in Army funding to buy new missiles and a 47 percent jump for the Navy’s weapons purchases.”

- “And none of this counts an estimated $18 billion of planned but now delayed weapons deliveries by the United States to arm Taiwan against a possible future attack by China.”

- “And there is $678 million to expand ammunition plants in spots such as Scranton, Pa.; Middletown, Iowa; and Kingsport, Tenn., where contractors work with the Army to manufacture the ammunition that Ukrainian artillery crews have burned through at an alarming rate.”

Years of Spending and Investor Potential to Come

Regardless of the politics, the war in Ukraine, one year on and perhaps many more to come, is a sinkhole for defense spending and a boon for defense stocks.

The USA is shipping massive amounts of weapons to Ukraine today. Many European nations are also depleting their arsenals for this cause.

It used to be what could be spared. It is becoming what is left. All of it must be replaced.

The USA is belatedly tooling up for a wartime economy. Perhaps one it isn’t fighting itself, but one it supplies and funds nonetheless.

It will be a multi-year, escalating surge, and there has rarely been a better time to invest in the kinds of stocks that make what’s needed.

Take care,

Adam English

The Profit Sector