On Friday, I told you I was on the verge of adding Meta (NASDAQ: META) to my “Favorite Trading Stocks” list. It’s a pretty short list right now, just two stocks – Aehr Systems (NASDAQ: AEHR) and StoneCo (NASDAQ: STNE).

The common thread that connects Aehr Systems and StoneCo is earnings…

Yes, both companies have substantial opportunities to grow their earnings from their respective sectors, which is always a good thing to look for in a stock to trade. But, especially in the current market environment, it’s not enough. Investors are wary because the possibility of worsening business conditions is very real. So only the cream of the earnings crop will attract the kind of attention that I want to see in a trading stock.

Both StoneCo and Aehr Systems are the cream, having posted recent earnings blowouts.

I feel like I’ve discussed Aehr Systems until I’m blue in the face. As a quick recap, I first locked into Aehr Systems back in early October. Shares were trading $14-$17 ahead of its Oct. 7 earnings report. Aehr crushed every metric, and the stock took off higher. Shares are just now moving above all-time highs set a year ago at $27.

And there is more upside for a simple reason: if the company can perform this well in a not-so-great economy, it’s reasonable to expect it to do even better when the economy gets on better footing.

The difference between Aehr Systems and StoneCo is that investors have jumped all over Aehr’s stock since that blowout earnings report. StoneCo, not so much. Shares of StoneCo jumped to the upper edge of the $10-$12 trading range it’s been in since October.

It hasn’t managed to break out yet…but that breakout is coming.

Stone Cold

The base case for trading/ owning StoneCo is very similar to that of Aehr Systems. That is, if it can do this well in the current environment, it should do even better when the business environment improves. And really, StoneCo could do even better than Aehr Systems…

Because StoneCo is a digital banking and payment processing company in Brazil. It’s like a more mature version of Square (NASDAQ: SQ) and its CashApp because it has deposit accounts. Brazil’s inflation problem is worse than here in the U.S., which has been a real millstone around StoneCo’s neck. But again, its recent earnings blowout tells me the company is lean and mean.

And the technical picture for StoneCo is a thing of beauty…

The so-called golden cross, where the 50-day moving average (purple line) has crossed above the 200-day moving average (black line), has happened. You can easily see the support that the 50-day MA (purple line, currently at $10.68) has provided since October. There is also good support at $11. And finally, there’s the resistance at $12. StoneCo has made several probes over $12.

None have stuck yet. But when shares do finally break over $12, a move to $15 could come in the blink of an eye.

The trading plan for StoneCo is pretty simple: I like call options with less than a month before expiration for the type of move I expect from StoneCo. Catch a 5% move for the stock with call options, and you’ll double your money. Catch a 10% move, and it gets fun. The best entry point would be on a dip to or below $11. The second-best entry is a break above $11.90.

The Case for Meta

It is very difficult for me to say anything positive about Facebook/ Meta and Mark Zuckerberg. I quit Facebook in 2015 because I hated it. The name change to Meta was an idiotic move by a naive egomaniac (note that the real brains of the operation, Sheryl Sandberg, left at that time).

And when I get sad, I have to think about the crybaby look on Zuckerberg’s face as he was firing 11,000 people via Zoom video because he “screwed up,” and I feel better.

I will say that Zuckerberg earned a couple of points in his favor by manning up and taking responsibility.

The simple fact is that any ad-driven business model will see its revenue gutted if and when the economy truly goes into recession. And while the U.S. economy hasn’t really hit the skids (yet?), Meta revenue will be down 1.6% this year, to $116 billion, and is expected to grow less than 5% next year – and no one will be surprised if revenue comes in weaker or even contracts again.

Of course, the real problem for Meta isn’t the revenue, it’s the amount of that revenue that’s getting invested in the metaverse thing. Earnings are expected to fall by 34% this year and another 17% next year. That’s bad, especially when the only justification for it is that the metaverse will be “really cool.”

But the thing is, the brutal beatdown the shares have taken now means that Meta shares trade with a trailing price-to-earnings (P/E) ratio of just under 12. And the forward P/E is right at 15. That’s pretty cheap. And it could easily get substantially cheaper if Meta cut its CAPEX and/or R&D spending.

Meta’s CAPEX spending jumped from $15 billion in 2020 to an estimated $27 billion this year. And R&D spending went from $18 billion in 2020 to an estimated $32 billion this year. With the stroke of the CFO’s pen, Meta could take ~$20 billion out of the expense column, add it to the net profit column, and that forward P/E would collapse from 15 to 7.

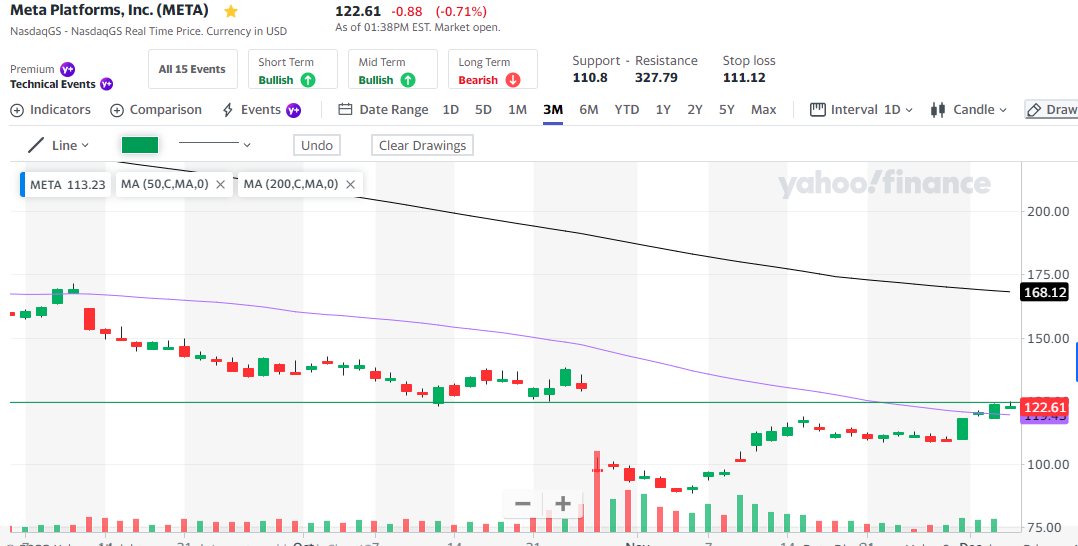

I think that the expectation that Meta will scale back its CAPEX and R&D numbers is why the stock chart looks…like…THIS!

I’m a simple man, and I like a simple chart. There are three things of note on this chart.

One, behold the green and red bars at the bottom. Each bar measures a day’s volume. Red bars are down the volume, green bars are up. Until that tall red bar, most of the bars were red, meaning that most transactions were sales.

But after the big red bar, it’s mostly green. Investors have been buying. And that buying has pushed the shares above the 50-day moving average (purple line). That’s the second item of note.

The third item is that the share price is hitting the horizontal green line that I added.

That green line is solid support/ resistance, right at $123. If Meta shares can take out that green support/ resistance line at $123, it will move into its old trading range, meaning it has a reasonable upside to $140.

And, as I said earlier, a well-timed call option trade should double with a 5% move. A 13% move could be worth 300%. So as much as I hate to do it, Meta (NASDAQ: META) is now in my trading sights. A re-test of the 50-day MA at $119.50 would make a nice entry point.

That’s it for me today, take care, and I’ll talk to you soon.

Briton Ryle

The Profit Sector