- Bonds Yields: $120 Trillion Could Never Stay Simple

- Stock Yields: The Fundamentals of Corporate Payouts

- Returns on the Return of Investment

- Do Not Catch a Falling Knife

- What Does It All Mean?

Once upon a time, or just a couple of years ago, virtually no one cared about high yields.

Oh, how times have changed.

We could go into all the reasons: Federal Reserve Fund Rate engineering, an unprecedented bull market, a prolonged stretch where corporate debt could be refinanced at bargain bin prices, etc.

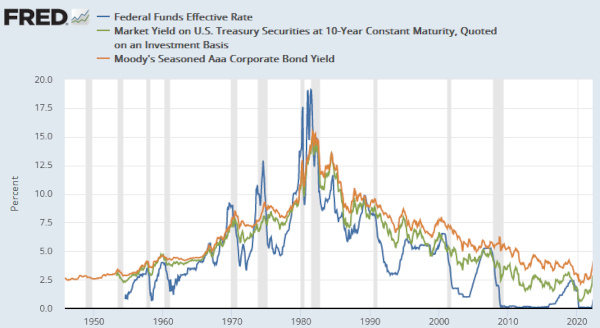

A chart shows it best without wasting too many words:

There is no singular definition for high-yield investments other than that they return a greater percentage of an initial investment than others.

For a long time, this relativity was retreating. What was considered a high yield kept falling over a decade of the Fed's “quantitative easing,” and, in reality, it has been going on for far longer.

Yields have been moving upward at a rate we haven't seen in decades this year, renewing investor interest.

A big part of it is inflation and the Fed's fight against it. The specter of a global recession looms, and investors demand a greater return to keep pace and generate consistent and constant returns in a time of uncertainty.

We need to make sure we know everything high-yield investments involve, though. We must understand how they are structured and the risks and rewards involved.

Let's get started.

Bonds Yields: $120 Trillion Could Never Stay Simple

First, let's get the first source of high yields out of the way – bonds.

The bond market is enormous and complex – estimates put it over $120 trillion – but its fundamental structure is not.

Let's start with the simplest version – bonds bought directly from a government or corporation as they are issued.

You pay a set amount. You are promised a yield, or percentage of the value, for letting the bond issuer use your money for whatever they want to do with it for as long as the bond exists. You get interest payments over the lifetime of the bond.

For example, say you buy a 10-year US Treasury bond for $1,000. It comes with a 3.5% yield these days. Twice a year, the US government will pay interest. Ten years with twice-yearly interest payments means whoever owns the bond gets one-twentieth of the 3.5% yield it guarantees over ten years when the government pays out. Then, at the end of the ten-year term, whoever holds the bond gets the $1,000 back.

However, only a handful of bond brokers and market makers can buy bonds at face value. Bonds get far more complex on the secondary market.

People may not want $1,000 bonds at 3.5%. They may demand more money over time for locking up that $1,000 for ten years. So they offer less than $1,000 to buy a bond with a face value of $1,000 at 3.5%. That increases the total return.

Maybe they're okay with a lower return that at least locks in any profit. In that case, they'd pay more upfront. That lowers the total return.

And nothing is stopping them from selling those bonds to other people before they mature but after collecting a lot of those interest payments.

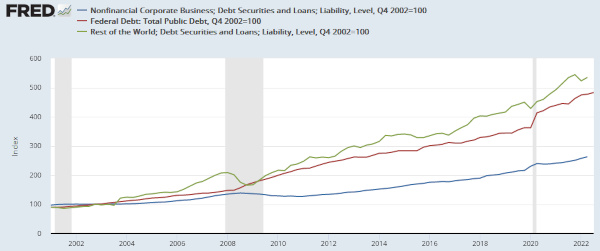

With $120 trillion or so on the line, the bond market could never remain simple despite its underlying structure. The yield and face value are technically static. The price you pay is not. The latter matters more to you than the former.

The bond market is big money on a global scale. Words cannot describe it, but a chart can, showing corporate debt up 250%, US federal debt up nearly 500%, and total global debt up almost 550% in just two decades:

I'll also mention a glaring exception with more complex securities like TIPS – Treasury Inflation-Protected Securities – where the principal (face value) and interest paid over time change inflation.

That's a whole different level of complexity and fodder for another article.

You also need to worry about the risk of bond issuers failing to make payments. Or other investors may not care to buy whatever bonds you're holding if you want or need to sell.

There are high yields in bond markets. They come with risks. The highest yield bonds are often illiquid, thus hard to trade and peg at a fair price. But if the issuer can meet its obligations, bonds will pay off in predictable ways.

Stock Yields: The Two Types of Corporate Payouts

Corporations issue bonds to take on debt they need to manage over time, but many also pay out of pocket to shareholders in the short term — some far more than others.

We can break these down into two categories: companies that return money to investors because of requirement or choice.

Profits Exceed Reinvestment

The first reason is not ideal, but it happens. Companies can find themselves in a spot where they are generating profits they can't easily reinvest into growth in the short term.

A prime example was Apple, Inc. (NASDAQ: APPL) about ten years ago. It was pulling in money at profit margins that it couldn't reinvest in its business. Shareholders wanted a return on their investment, though.

It kicked off a period of large dividend payments. It had yet to pay a dividend since the 1990s before it nearly died.

From August 2012 to May 2014, it kicked cash out to shareholders at an accelerated rate. It repurchased its shares and split its stock twice too.

It still sits on a mountain of cash, but the share buyback program has been massive, hitting a record at nearly $90 billion in fiscal 2022. Tech stocks are a mess going into 2023 but still awash with money.

A more recent example is ConocoPhillips (NYSE: COP). ConocoPhillips paid out $1.40 per share on October 14th, 2022, on top of a $0.46. quarterly. That's a full year's payout in one quarter.

Many smaller companies never intended to grow into these kinds of massive companies.

We'll get to that later, and it's a potentially lucrative market that depends on stability and free cash flow.

Company Structure Demands It

The other case – the legally obligated – kicks in when the company structure demands it.

For myriad reasons, some companies build themselves in a way that minimizes taxation and passes on that obligation to shareholders. That increases the cost of owning shares of these companies but comes with strict rules.

The most important is nearly universal – they are “pass-through entities” where the income they gain goes straight to shareholders as dividends (technically disbursements).

Real Estate Investment Trusts – or REITs – and Master Limited Partnerships – or MLPs – are the two common ones.

There are differences between them. REITs must pay out 90% or more of their income to shareholders. MLPs do not have this obligation, but they often do because the people that own them – technically unitholders instead of shareholders – demand it.

Another difference boils down to what industries these niche corporate structures do.

REITs, as you can imagine, deal with real estate income. MLPs are a bit more convoluted and heavily concentrated in the energy sector – especially pipelines and “middle-man” distribution businesses.

We'll keep covering these, as we have before. REITs and MLPs consistently return high yields to investors and will always be featured in high-yield dividend lists.

Returns on the Return of Investment

Besides windfall profits and required payouts, some companies do a great job of making their owners some money as they chug along.

Some are now massive, and some serve niche markets, but one thing ties them together: consistent results and free cash flow.

What we're looking for with these kinds of companies are net profits that easily exceed debt obligations and aren't needed for debt management or transferred to capital expenditures.

Major oil and energy stocks stand out in this market corner. I've mentioned some of them worth watching in 2023. That's more a product of the bullish energy sector – a very volatile one that may not fare well in 2023.

The yields from these companies have diminished as their stock prices have risen. That's bound to happen. Elsewhere in the stock market, some big names have big payouts.

Verizon Communications Inc. (NYSE: VZ) has a yield of over 7% after a pullback in share price over the last several years. Same for AT&T, Inc. (NYSE: T) at 5.8%.

If you don't mind investing in a “vice stock,” Altria Group, Inc. (NYSE: MO) has a nearly 8% yield.

The inverse can also happen, and we need to talk about it.

Do Not Catch a Falling Knife

You might have skipped right by it – and I can't blame you – when we talked about bonds, but the relationship between “face value” and yield affects stocks too.

Sure, there is no actual guarantee for bonds. They come with the risk of default, but creditors – such as bondholders – are at least pretty high in the pecking order after a corporate collapse.

That is different with shareholders. There is no guarantee of any return – not implied and certainly not built into an investment. Not for the yield, not for the stock.

Be very careful with companies with falling revenues and free cash flow. They'll show a high yield, but many can never deliver results.

For example, and to reuse the examples above, Verizon Communications Inc. (NYSE: VZ) has seen its yield increase because its share price has fallen 27% over the last five years. AT&T, Inc. (NYSE: T) has seen a 30% drop over the same timeframe.

Verizon and AT&t are not failing companies. But they are struggling with revenues and free cash flows, which has weighed on share values. Nothing prevents them from slashing their dividend yields.

Here is an extreme example. ZIM Integrated Shipping Services Ltd. NYSE: ZIM) is down nearly 78% from its high in March 2022 and shows a trailing 12-month dividend yield of over 60%.

There is no version of any company that pays out over half its market capitalization to investors per year.

It is a falling knife. The data for its dividend yield is trash.

ZIM is an extreme example, but lesser versions play out all the time.

Sorting through stocks for high dividend yields must include an in-depth look at free cash flow, debt burden, and credible forward projections.

What Does It All Mean?

We've covered a broad scope of topics related to getting a high-yield return through interest or dividend payments from investments.

It's worth a recap with one thing in mind – it's all about structure.

Bonds play by their own rules, and you need to be aware of that, especially in the secondary market.

Corporate structure matters a lot with stocks, especially with REITs and MLPs. High yields mask extra tax concerns.

Stocks owe you nothing. Windfall profits from energy stocks won't repeat. The bonanza is limited, and share prices and yields may drop in tandem. There are no guarantees here.

Free cash flow is vital. Companies that can offer high yields consistently build up the cash they need to make the payments.

“Falling knife” stocks can be a double whammy. Their share prices drop, and their dividend yields appear to soar based on past payouts. It is unsustainable, and share prices and dividend payments drop in tandem.

Plenty of investments out there will consistently return money to you if you're a shareholder… provided they have the potential for growth. With interest rates rising, it will be challenging, but it's more important than ever.

We'll keep covering the sector and keep you informed about the best of them.

Take care,

Adam English

The Profit Sector