- Old Ideas, New Tech

- The Birth of “Fintech“

- Fintech’s Growing Concerns

- A Fintech Company to Watch – SoFi Technologies, Inc. (NASDAQ: SOFI)

Fintech has lost some of its luster. Nothing could be better for new fintech investors.

It no longer grabs headlines when a start-up CEO includes it as a buzzword in a slide deck for a tech conference presentation.

It can no longer leech off of any mention of blockchain integration or app development.

It needs to start delivering on promises, some over a decade old.

While it may be brutally volatile, in this era of suffering tech stocks and rising interest rates, fintech is finally entering a second phase. One where hype helps, but results reap the rewards.

Let’s dive in and look at how fintech has evolved, it's recent reckoning, and where it goes from here. Plus, let’s look at an intriguing company.

Old Ideas, New Tech

Fintech addresses a need as old as time. The tools it uses are perpetually new, by definition, but don’t be fooled. Its goal aligns with banks and money lenders going back to the dawn of commerce.

Maybe I’m “of a certain age,” but here is some of the first “financial technology” I remember:

Drive-through banking used these capsules in pneumatic tubes to push documents back and forth. Deposit and withdrawal slip, cash, and cashier’s checks. Lollipops for the kids.

They also did a lot more in bank-to-bank transactions. Here is a picture from 1943 of a much more complex system that used those old things:

This is fintech at its heart, in an anachronistic format that is now laughable. Yet the goals of this are the same as those of fintech today.

The only defining traits of “fintech” are data fidelity and speed.

There was a time when pneumatic tubes for paper copies – often carbon paper, inevitably in triplicate – gave a clear advantage to those that used them.

One quickly followed by ‘yes or no’ phone line approval for consumer lines of credit, soon followed by ATMs as debit cards were issued.

In 2009, Paul Volcker – former head of the Federal Reserve – famously stated when asked about reforming financial services:

“You are not going to be very happy with my response… The only useful thing banks have invented in 20 years is the ATM.”

This is both a validation and critique of fintech that resonates today. Fintech continues to improve upon technological advancements that have a long arc. Better access to services by customers, better loan origination without making someone reference an actuarial table, better data to mitigate risk, etc.

It also can be used to gloss over risky financial products that tap into what once were hard-to-access investments like options, other derivatives, and new investments like cryptocurrencies.

It has moved from a yes or no question – “does this account exist, and is there enough money in it?” – to far more complex forms of finance.

The Birth of “Fintech”

Fintech, as we know it now, came about as computers took over more and more complex tasks.

Loan approval and payments, mortgages, matching lenders to lendees in near real-time, and big data analysis have all taken off.

Insurance companies have hopped on board and can issue accurate quotes not only for a single service but compare different tiers across multiple insurers with just some basic consumer information, all through one platform.

Fintech has developed deep ties to online brokerages and blockchain technologies like cryptocurrencies. Big data, cloud computing, and artificial intelligence are integral.

And virtually all of it is completely designed to avoid human interaction beyond apps and website portals.

The result is far faster and cheaper processes. Like in the days of pneumatic tubes, the goal is to use the best data available at the fastest possible speed.

Investment in this technology has soared through start-ups and established brokerages, insurers, and banks.

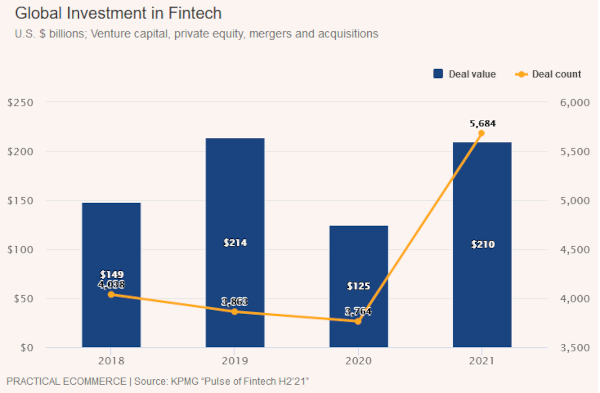

Global investment is estimated to have grown from $930 billion in 2008 to $210 billion in 2020, with an all-time high of $214 billion in 2019. That’s a nearly 12,000% increase.

Fintech’s Growing Concerns

This growth, unfortunately, has also fueled growing concerns.

First is increased attempts at fraud through identity theft, data breaches, and hacking business transaction protocols and databases.

Even something as basic as a distributed denial of service attack, where a bunch of computers is used to flood servers with useless information requests at extremely high speeds to choke them and bring them offline, is a massive concern due to how it disrupts fintech businesses.

Then there are the implications of seemingly more mundane concerns that financial institutions and service providers have faced since the dawn of time.

Fintech grew in an age of unprecedentedly low-interest rates. An environment rapidly changing across the world.

Fintech companies may ultimately lower costs and drive more business, but the financial services are capitalized in the same way they always have.

Though they may be originated in novel ways, loans still need to be collateralized. A business still needs the capital to back up the money its customers borrow.

Many fintech companies act as matchmakers, but they functionally have their limits placed on them by the underlying banks they work with. Once those limits are met, matchmaking and profit-sharing deals with the banks can’t continue, and revenue streams dry up.

This can be a quick path to insolvency for companies that already have high start-up costs and run on negative net revenue through issuing more shares and enticing shareholders to buy more.

Plus, in recent years, we’ve seen artificial intervention. Think of the moratorium on student loan payments and evictions where revenues are not collected due to nonpayment.

The societal value of this was real. We’re coming out of several years of a pandemic where – for better or worse – you be the judge – and there was some logic to freezing costs for people that were forced to lose wages. Yet the cost to lenders or “middleman” businesses, like many fintech companies on the other side of the equation, were immense.

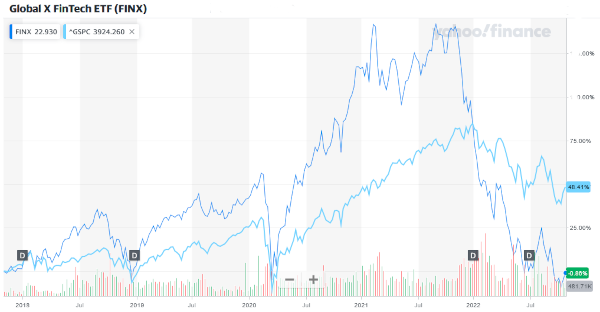

In 2022 in particular, amidst a large and long tech sell-off, fintech has seen the last five years of stock market gains erased, at least when using the Global X FinTech ETF (NASDAQ: FINX) as a proxy, with the S&P 500 index added for comparison to the broader market.

A Fintech Company to Watch

That gets us back to what was mentioned at the top of this article. Nothing could be better for new fintech investors. The bubble has popped, and fintech is now trading in line with other parts of the tech sector at much more reasonable valuations.

In the meantime, those five years weren’t lost. Several companies have seen massive growth and technological improvements that will drive revenues going forward.

We’ll skip right over some of the largest companies. These days, Visa (NYSE: V) and Mastercard (NYSE: MA) technically count as fintech in their own way. Then there are established companies like Stripe, Paypal (NASDAQ: PYPL), and other payment platforms.

Instead, we’ll look at a decade-old company that is well positioned either as a takeover target or can go it alone with its growth potential compared to its peers.

SoFi Technologies, Inc. (NASDAQ: SOFI)

SoFi Technologies, Inc. (NASDAQ: SOFI) is a San Francisco-based company founded in 2011 that focuses on student and auto loan refinancing, mortgages, personal loans, credit cards, and banking through mobile and more traditional desktop apps.

It was a darling of venture capitalists, raising billions in private investments before going public through a reverse merger with a special purpose acquisition company at the end of the first quarter of 2021 at a $9 billion valuation.

Since then, it has seen its market capitalization halved and shares down about 70% from the IPO, in line with the sector-wide pullback mentioned above.

After an early start that used a unique model to connect current students at specific schools with alumni and institutional investor lenders, the company has expanded into a much broader portfolio of loan types and mobile banking that retained a no-fee system that pulls revenues from interest alone.

Personal, student, and home loans are available. Through partner banks, its mobile banking platform is FDIC-insured. It acts as a matchmaker for third-party insurers and bundles in a credit score monitoring and budgeting tool. Plus, it offers cryptocurrency and stock investing services.

It also was severely impacted by its exposure to the moratorium on student loan payments. However, that risk appears to be about to end.

As a result of the pullback, its growth rate and low valuation make it a fintech stock to watch.

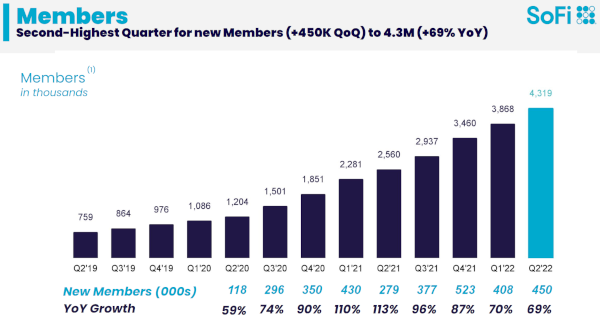

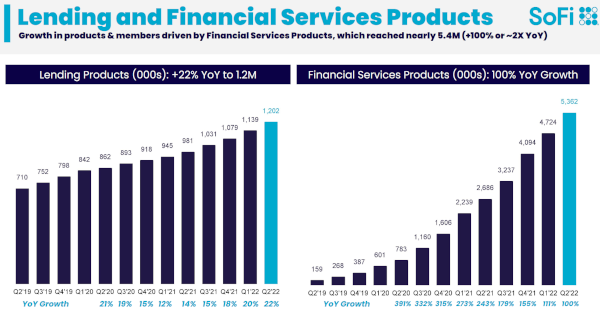

Second quarter 2022 growth rates saw a massive 50% growth in revenues and membership growth of nearly 70% year-over-year.

More importantly, SoFi has seen substantial growth in the products its members are using. The members it brings on board are driving revenue growth by using more products than they initially signed up for, driving product growth at an ever-increasing rate.

It has managed this while shrinking its net losses by nearly half – $96 million versus $165 million year-over-year for the quarter.

SoFi also acquired a banking charter by acquiring Golden Pacific Bancorp this year, which is a significant advantage over peers and is benefiting from its acquisition of Galileo, banking as a service platform, in 2020.

Deposits quickly rose to $2.7 billion in Q2 2022, marking a 135% year-over-year surge. This drives better earnings and margins while driving down risk and per-customer operating costs.

SoFi checks all the boxes investors are looking for in the sector. It is using mobile apps to reach the greatest possible range of consumers. It uses AI and big data to offer loans and financial services in near real-time, and its portfolio is constantly improving to mitigate risk.

It is a fantastic potential turnaround play in a beaten-down sector, though it remains a high-risk, high-reward investment, like all of its competitors.

The company needs to maintain high growth rates while continuing to rein in operating losses. It also may need to do this with continuously increasing interest rates and with a risk of an economic slowdown impacting its lending operations.

If it can do this, within a matter of years, it can produce results that will justify share prices several multiples above where they are now.

Take Care,

Adam English

The Profit Sector