“If you don’t know where you’re going, you’ll end up someplace else.”

– Yogi Berra, Hall of Famer

Let's play ball!

This is one of my favorite times of the year: green grass, warm breezes, and the start of baseball season.

I’ve been coaching my son’s little league baseball team for several years now. For my money, there are few things as pure and invigorating as playing ball on a spring evening with a ragtag group of 11-year-olds with only a firm grasp of fundamentals and an endless well of energy.

It is also a reminder that vital skills like patience, attention, and retention allude not just to kids playing a game but to investors at large.

One glaring mistake that my sluggers-in-training continued to make was their approach at the plate. It was quite clear that despite most of them weighing in at around 75 pounds, when they swung the bat like the second coming of Babe Ruth. The bulk of the team was swinging for the fences with every pitch and whiffing on about all of them.

But there was one kid who consistently made serious contact with almost every pitch simply because he had a measured, level swing. He never tries to muscle the ball out of the park. He treats every at-bat like it’s his first instead of his last.

He ended up having the best batting average on the team.

Much as I’ve advised my readers to take investing slow and steady with positions like dividend aristocrats, I’ve also advised my son that a single or a double is monumentally better than risking a strikeout for that rare home run.

But once in a while, if you see a good pitch to hit, we’ll take a swing at a home run stock. We’re not focused on one at-bat or even one game. I’ve positioned my portfolio to contend for an entire season and lead us to everyone’s final goal — the World Series – or in our case, a championship retirement.

In baseball and investing, it’s always better to take a walk than strike out.

Here’s how to grow your investments into a field of dreams…

The Single: ProShares S&P 500 Dividend Aristocrats ETF (BATS: NOBL)

Let’s start with the humble single. It’s the key to starting off a game and anchoring a portfolio. I’m going to recommend a safe dividend stock with a modest but sustainable yield.

It also happens to be an ETF.

My favorite ETF is the ProShares S&P 500 Dividend Aristocrats ETF (BATS: NOBL). It tracks 50 companies in the dividend aristocrats index (companies that have raised their dividends 25 years in a row). It’s a big fund with $11.66 billion in assets, a reasonable expense ratio of 0.35%, and a 1.92% dividend yield.

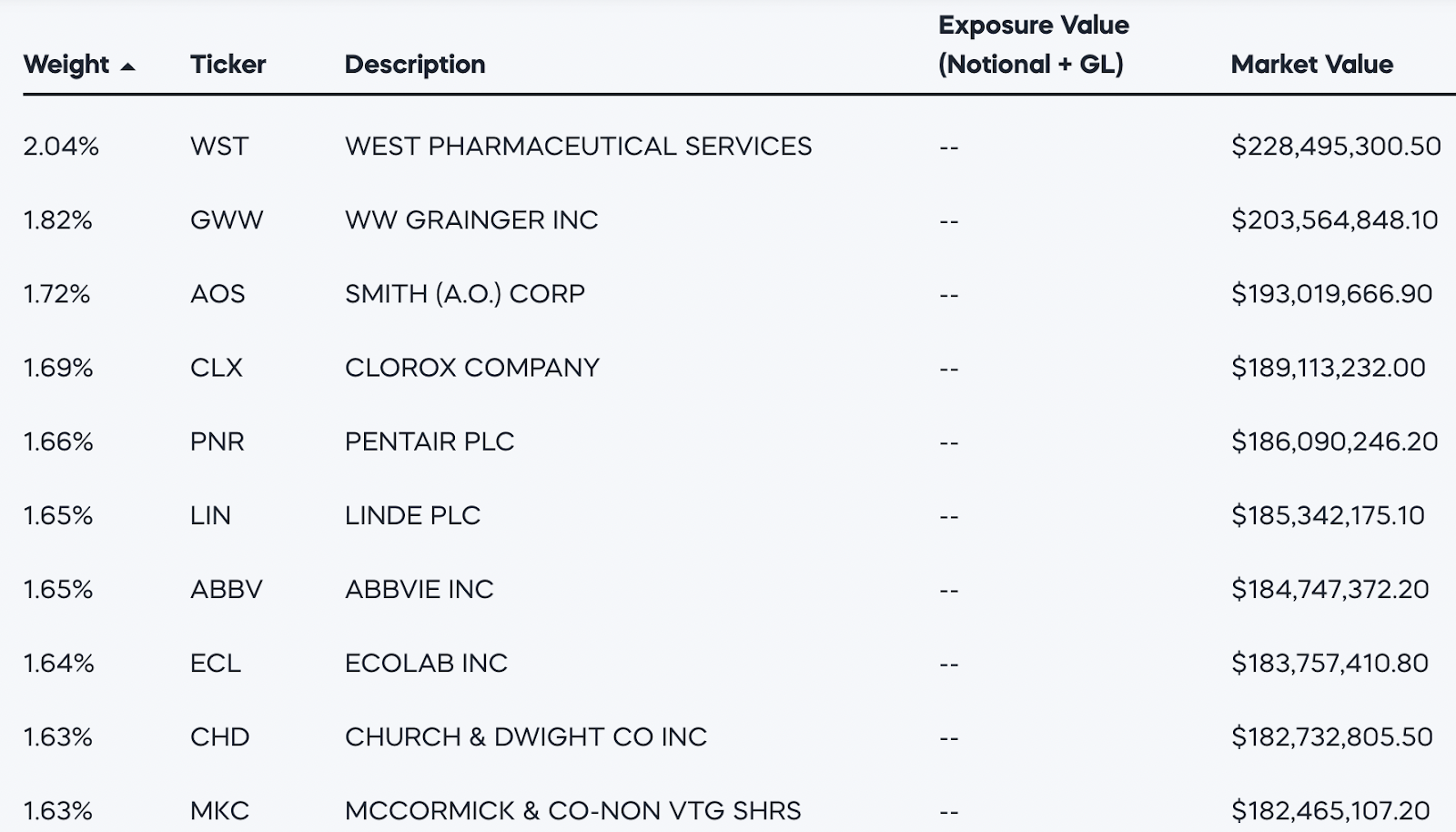

Here are NOBL’s top ten holdings:

As you can see, it’s very diversified, with dividend-paying companies in all sectors.

NOBL will get you on base every time and – over time – steal you a couple of bases and set up the rest of the lineup.

*Pinch hitter: SPDR Portfolio S&P 500 High Dividend ETF (NYSE: SPYD)

The Double: Otis Worldwide Corporation (NYSE: OTIS)

While NOBL is an easy bunt single, I’m looking at one of their newest holdings as an easy, stand-up double.

It never occurred to me to invest in elevators, and despite OTIS holding the title for the largest elevator company in the world, I had honestly never taken note of the name in the hundreds of elevator rides I took until I got trapped in one, alone, for almost an hour.

Editor’s Note: Being trapped in an elevator is actually pretty cool if you aren't completely claustrophobic. It will either turn you into a raving maniac or a trappist monk. The personal reflection time was very valuable for me, and I got a stock pick out of it.

Next time you’re in an elevator, I bet you’ll see that OTIS logo staring back at you.

It’s funny how you can overlook such things until something else prompts you to do so. In any case, still believing it was a sign of some kind, I began doing my due diligence on Otis Worldwide Corp., and it looks like a great “single” stock.

Otis manufactures, installs, and services elevators and escalators in over 200 countries. Founded in 1853, they’ve been taking passengers up and down for over a century and a half.

The company operates through two segments: new equipment and service. The new equipment segment designs, manufactures, sells, and installs a range of passenger and freight elevators, as well as escalators and moving walkways for residential and commercial buildings.

The service segment performs maintenance and repair services, as well as modernization services to upgrade elevators and escalators.

Otis moves two billion people a day and maintains more than two million customer units worldwide.

The reason I hadn’t noticed them in my years of dividend aristocrats research is that they were recently grandfathered into the elite group. Otis was spun off in the merger of United Technologies and Raytheon (NYSE: RTX). They were able to keep the designation based on both companies’ dividend history.

The company sports a $33.68 billion market cap and a modest dividend of 1.38%. Otis Worldwide’s annual revenue for 2021 was $14.298B, a 12.09% increase from 2020. They employ 69,000 people.

I don’t think they’re going anywhere but up; it could be a nice long-term dividend play because we’re going to be using elevators, escalators, all of those things for the time to come. Every building needs one for practical reasons, but they are also mandated by the Americans With Disabilities Act to make sure the building is handicap accessible.

So if a building is at least three floors, it has to have, by law, an elevator. It’s always great when the government mandates your product be sold.

More importantly, Otis makes the bulk of its revenue in the service sector. Elevators are in constant need of maintenance and repair, and Otis’ service segment makes up 60% of their sales and 80% of operating profits.

That backstop of service business is crucial for economic downturns. In fact, despite the shutdown of most major office buildings last year due to the pandemic, shares of Otis soared nearly 55% in 2020, and the company merely posted a slight decline in organic revenue growth during a pandemic-impacted year. With things opening back up and more construction set to take place to keep up with increased urbanization, Otis should have much more profitable years in front of them.

As I said, the dividend is only around 1.38%, but they’re forecasted to grow about 6% a year. Now that they’re part of the exclusive dividend aristocrats club, they aren’t likely to risk getting booted out anytime soon. They have a targeted ~40% dividend payout ratio, which allows for some breathing room in the future.

Eventually, you could be collecting a few bucks in cash payments per share for the next decade.

Otis Worldwide Group (NYSE: OTIS) won’t make you rich overnight, but it is a solid addition to a retirement dividend portfolio.

And you’ll always have a runner in the scoring position.

Pinch Hitter – Essential Utilities (NYSE: WTRG)

The Triple: Illinois Tool Works (NYSE: ITW)

Illinois Tool Works was founded in 1912 by Byron L. Smith. Smith put out an ad in the Economist, looking to provide capital to a “high-class business (manufacturing preferred) in or near Chicago.”

He turned down several initial offers, waiting for the right proposal. And when a group of inventors with an idea to improve gear grinding came along, ITW was born. It continues to rule many more spaces today. ITW manufactures and sells industrial products and equipment worldwide.

It operates through seven segments:

- Automotive

- Food equipment

- Test and measurement and electronics

- Welding

- Polymers and fluids

- Construction products

- Specialty products

It’s now one of the best-performing dividend stocks of the last century. It’s flourished through wars and recessions and has expanded its businesses around the world.

The company is not only a dividend aristocrat; it’s also a dividend king. This means that it’s had over 50 years of consecutive dividend increases.

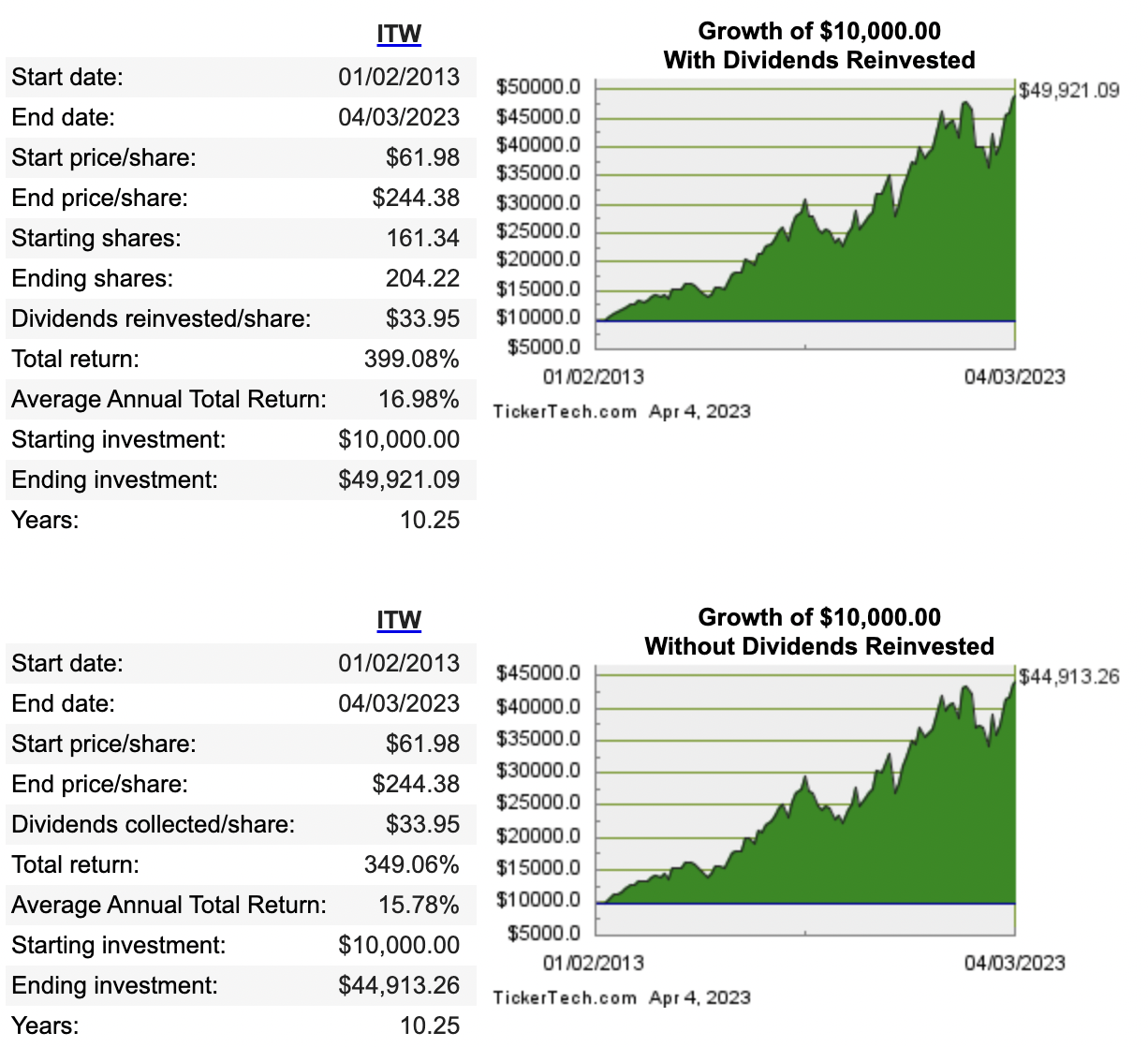

Had you invested, here’s how you’d have done with ITW over the past decade:

That's literally tripling your money (almost quadrupling it if you reinvested your dividends).

ITW is up 5% compared to the S&P 500 (down 11%) and the Nasdaq (down 14%). They also posted a record Q4 2022 operating income. That strength allowed them to raise profit estimates for the year.

It’s a rather recession-proof stock as it supplies crucial products to some of the largest companies in the world.

Given all of that, I would happily slot them into the number three spot in my lineup.

ITW currently yields a respectable 2.14%.

Pinch Hitter – Stellantis (NYSE: STLA)

The Home Run: Bluebird Bio (NASDAQ: BLUE)

This stock would be your clean-up hitter, which is typically a big slugger that is as likely to strike out as he is to hit a home run.

As part of an antifragile portfolio – where you allocate 80% of your investments to “safe stocks,” as I featured above, and 20% to high-risk investments, your home run hitter would fit into the latter category.

That includes investments like crypto, biotech, and junior miners. You need to be able to tolerate the risk of losing it all – or hitting a moonshot. I’ve done both in my years as a cannabis investor, where I made readers as much as 3,000% but struck out on several penny stocks. Overall, however, I made way more money on my homers than I lost on my strikeouts.

For our home run hitter, we need to look at small-cap stocks.

Let’s slot Bluebird Bio (NASDAQ: BLUE) into our clean-up spot. Bluebird is a clinical-stage biotechnology company, a sector that is notoriously sink-or-swim. It’s relatively tiny, with a market cap of just $323 million.

Bluebird’s focus is on gene therapy research and development, which is an emerging field just entering the public’s purview. It involves the genetic modification of cells in order to prevent or treat disease by repairing defective genetic material.

It’s the stuff of science fiction, and that’s why investing in this space is a risky maneuver. A company would have to clear several regulatory hurdles and pass a number of trials to get its products to market.

And it could take quite a bit of time…

The key to short-term investing in industries like this is the trials. When a company hits on a trial, the stock rallies big time. When it misses, the opposite is true. As far as gene therapy goes, these trials have been going on for decades now – from 1989 to 2018, there were over 2,900 clinical trials, half of them only reaching phase I. It wasn’t until 2003 that the first gene therapy company got regulatory approval.

However, that’s why Bluebird could be a home run in the near future.

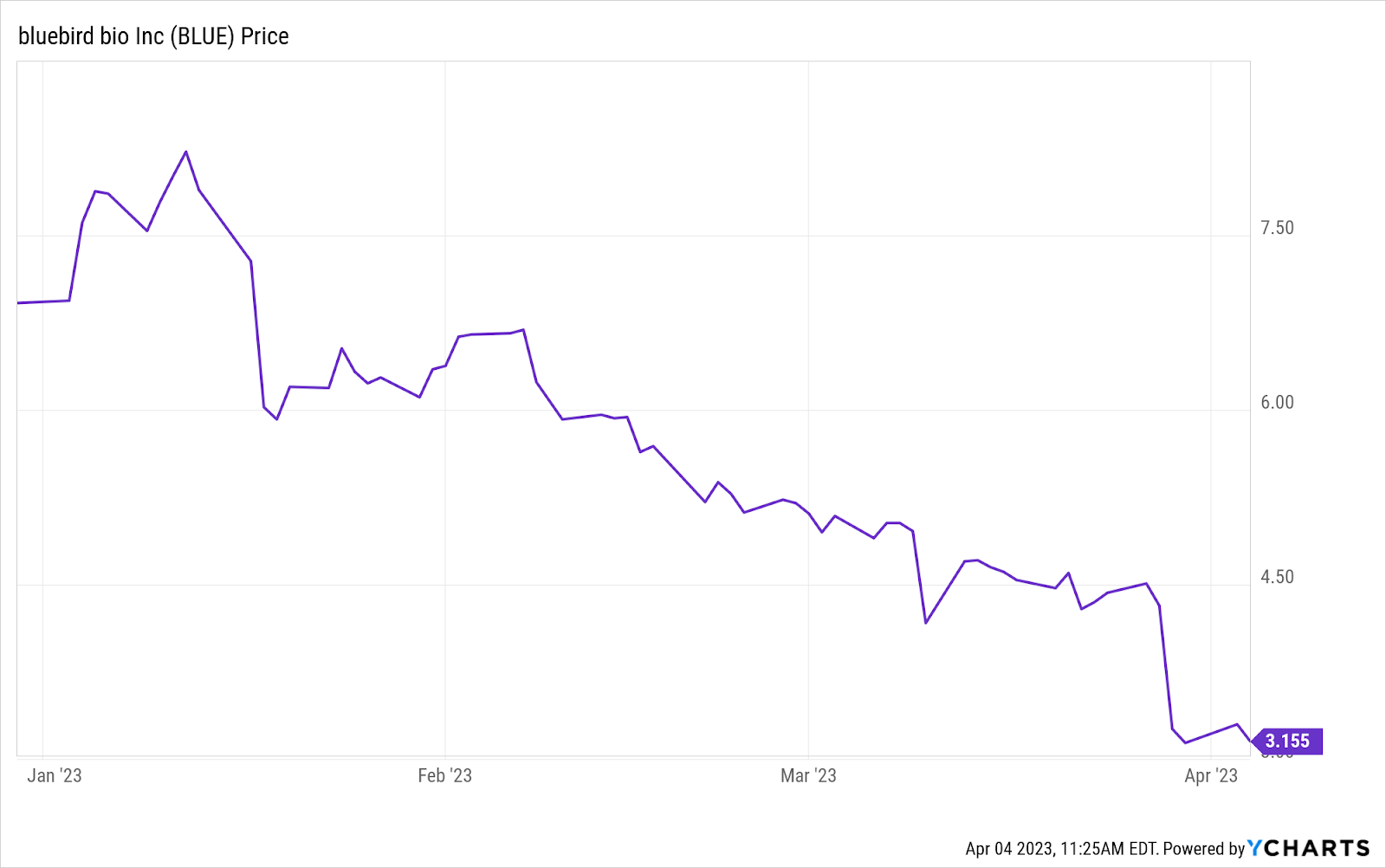

They lost over 50% of their share price. That’s the world of small biotechs taking on some of the most important and difficult problems in the world.

I’d say if you want to take a swing at something, Bluebird has the research team, the cash, and the name recognition to pull off a successful trial or two. It doesn’t hurt that the company is pursuing some very rare disorders that cost an absolute fortune to treat.

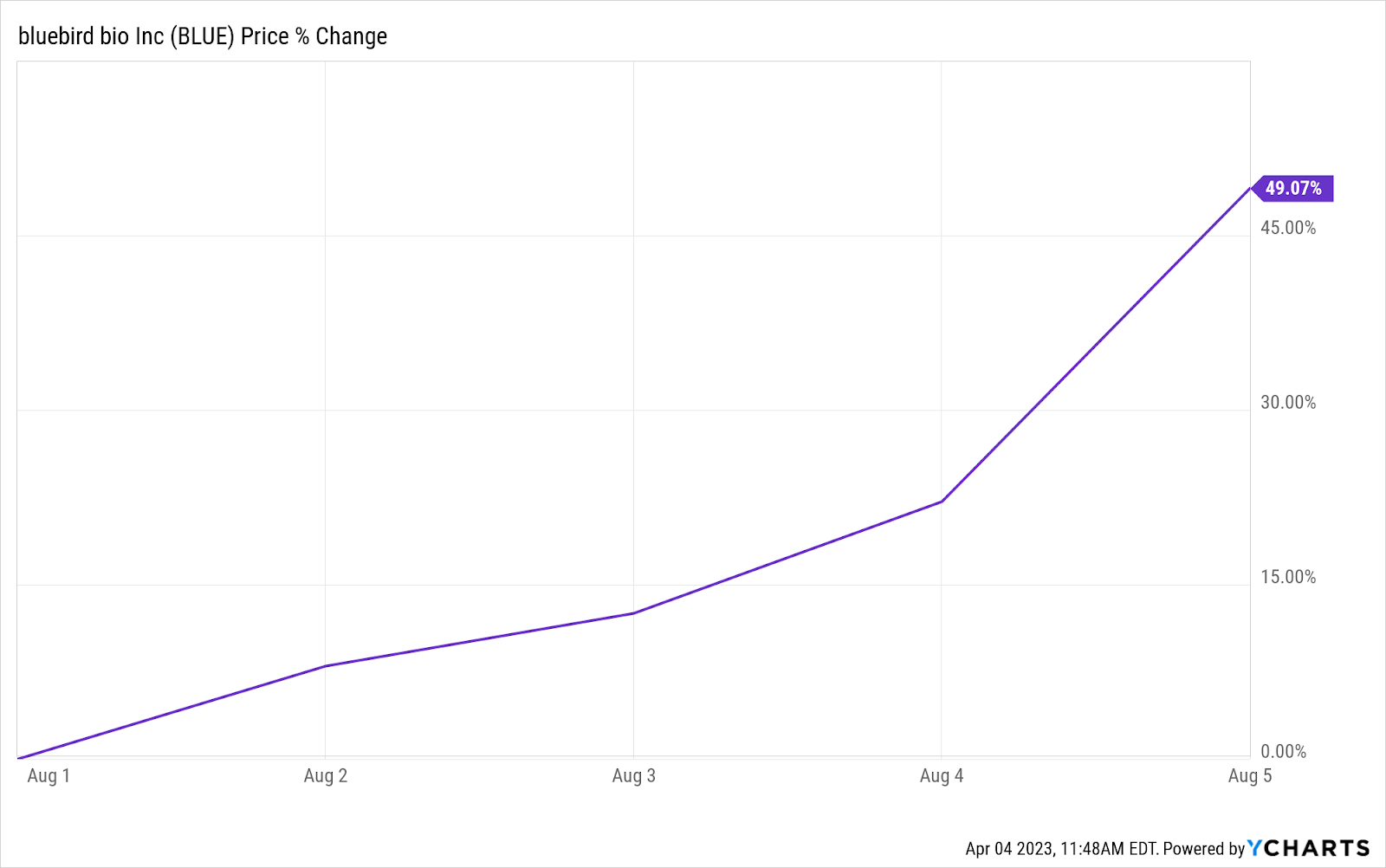

Bluebird’s treatment for TDT – a very rare blood disorder – Zynteglo, was approved last summer and had the controversial title of the most expensive treatment in history at $2.8 million.

After the approval, the stock shot up almost 50% in less than a week:

That’s a heck of a return in a couple of days, but look at what the company has done since the beginning of the year:

That is despite the fact that Bluebird was also able to beat their own record for the most expensive drug in the world when Skysona – a treatment for the neurodegenerative disease CALD (cerebral adrenoleukodystrophy) was approved. That drug goes for $3 million.

While those two approvals sent the stock soaring, the market is much more of the “what have you done for me lately” type.

As far as Bluebird goes, it appears that those two drugs alone will start to pay off big time. The company is anticipating up to 1,500 patients with Zynteglo and another 50 patients with Skysona. That would add up to billions of dollars when they start posting financial reports next year – another catalyst for small biotechs like this.

I’d be buying on the recent dip in anticipation of the company beating revenue over the next year.

But heed my warning as a Baltimore Orioles fan – companies like Bluebird could end up in a Chris Davis situation, where they hit two big slams, get attention and a big contract, and immediately begin striking out half of the time going forward.

Make sure you have a balanced lineup if you seriously want to compete in this market and against the competition for years to come. As Hall of Fame baseball coach Tommy Lasorda once said, “There are three types of baseball players — those who make it happen, those who watch it happen, and those who wonder what happens.”

The same goes for investors.

My advice? Make it happen.

Godspeed,

Jimmy Mengel

The Profit Sector

Follow me on Twitter @mengeled