- The Resilience of Fossil Fuel Resources

- The Bullish Case for Oil

- The Bullish Case for Natural Gas

- How to Profit from Oil and Natural Gas Going Forward

We're going to talk about natural gas and oil. We have before, and the analysis holds up pretty well, but it's time to dig in yet again.

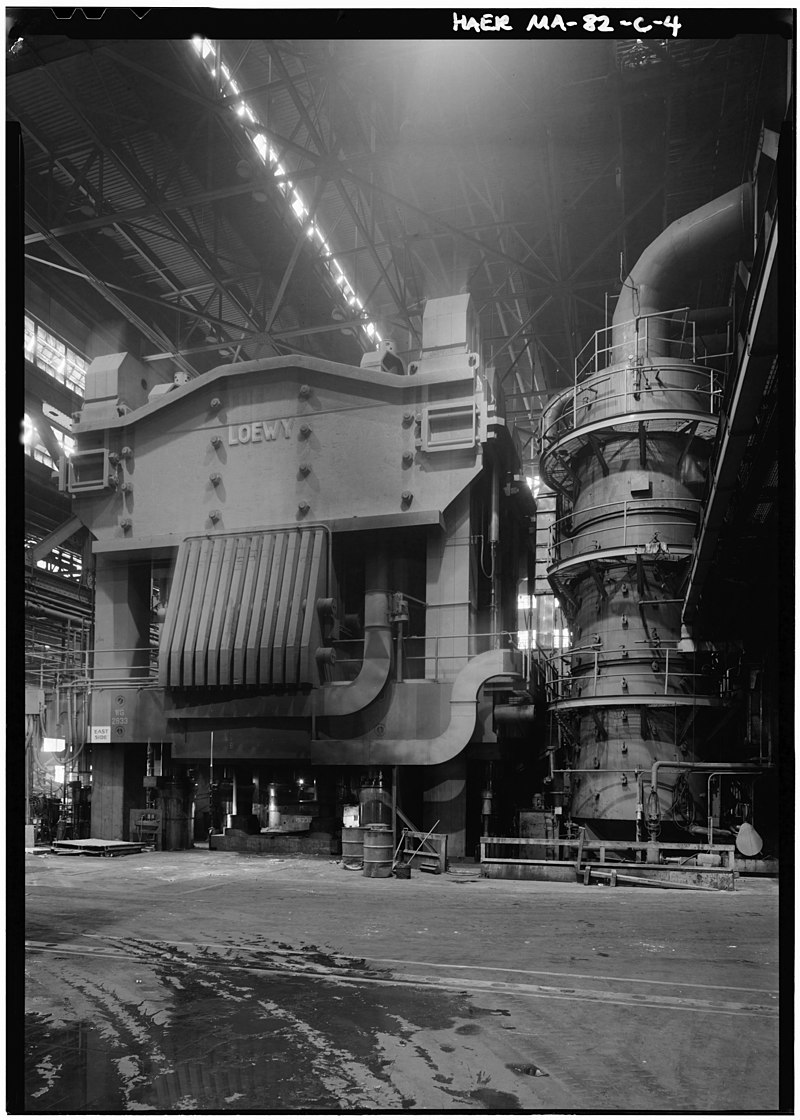

First, I'm going to “bury the lead” and ask you to look at this glorious monstrosity.

It'll drive home a critical point.

There are a pair of oil drums for scale upfront. They're a bit under 3 feet tall, so half a person.

What are we looking at? It's a 50,000-ton forging and extrusion press, affectionately called “The Major,” commissioned during World War II by the government. It started production in 1955 and is one of a handful of unique machinery still in use today.

Some others are larger, including an 80,000-ton forge in China. If you want to read a great article about these old 50,000-ton behemoths, here's one.

What does that have to do with oil and natural gas? It's a prime example of a relic and role we can't ignore. That we still depend on.

It is still one of New England's largest single natural gas users, comparable to 8,000 Massachusetts households.

Now I'm going to get to the crux of the matter. How do you think this whole energy paradigm transition works?

How do you think a battery that can power 8,000 homes works? How do you charge and discharge power to it daily?

These are questions that should be at the forefront of any attempt to replace fossil fuels.

Their implications are already playing out in the energy and stock markets and will for years to come.

The Resilience of Fossil Fuel Resources

I've picked one example of something that cannot be retooled and demands immense on-site power.

It is just one of the most extreme. There are a lot more that are more mundane but add up to a constant level of demand.

Steel foundries depend on it. Concrete production does as well. Plastics, metals, and even solar panel production with silicon-based semiconductors; all depend on extremely high temperatures that are best fueled by natural gas.

The same goes for vehicles. Diesel fuel trains and trucks are a big target for EV replacement, but what is on the road now will persist and drive demand.

Hauling along the weight of batteries that can provide the immense power they require is an engineering nightmare. Technically, discharged batteries weigh a bit less than charged ones, a little nerdy E=MC2 physics fact, but it's nothing compared to burning off all the fuel as you move along.

Natural gas and oil matter. They will well into the most aggressive clean energy paradigms, and in a world with inflation and energy insecurity, doubly so.

That's why we're seeing oil prices remain resilient. That's why they are expected to rise again even after the steep drop in natural gas prices in recent months.

These are cyclical and resilient energy sources, and these are resilient investments. Something the economy, businesses, and investors remember now more than they have in a long time.

Let's look at what supports both fuels now and in the future, one at a time.

The Bullish Case for Oil

First, Saudi Arabia and other major oil producers decided to cut oil production by over one million barrels per day, starting in May and running through the end of the year.

To put that in dollars and cents, The Department of Energy predicts the summer seasonal increase at 32 cents per gallon on average.

It isn't big in the grand scheme, working out to about 1% on average, but it is a big move by OPEC+ nations after a year of cautious and highly politicized moves in a market with tightly balanced supply and demand.

It also doubles down, figuratively and not literally, on cuts to production in October of about 2 million barrels per day.

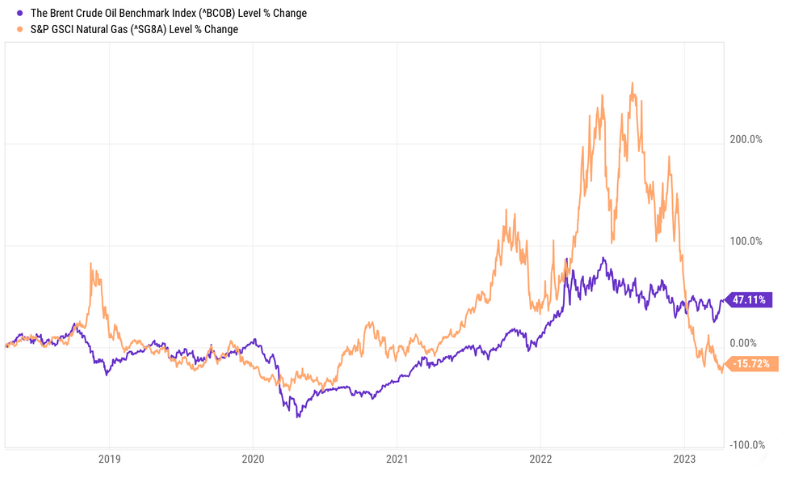

Looking at a five-year chart, you can see why they'd want to protect current prices as much as possible. Oil prices drop nearly two-thirds in the Brent Crude Oil Index within a couple of years, then soar upwards:

As you can see, I also tossed in an S&P GSCI Natural Gas Index line. The price action there has been wild.

There has been a severe drop in prices, but that only reinforces a bullish market.

The Bullish Case for Natural Gas

After the initial fallout and speculation about the winter reserves in highly dependent Western Europe, natural gas global prices have plunged. Regional differences are still significant, and arbitrage plays are still possible, but they aren't what they were.

This may be a short reprieve…

As covered by Reuters, the race is already on to secure next winter's supply, and it looks just as tenuous as it was for the last.

In 2022, Europe (specifically the European Union bloc of nations) imported 121 million tonnes of liquified natural gas (LNG) in 2022, a 60% increase year-over-year.

As EU citizens can attest, that came at a steep cost. Most of that buying action went through the spot market. That tripled costs to $190 billion.

Analyst estimates suggest how large of an increase that was on a global scale, with the EU accounting for 33% in 2022 versus 13% in 2013.

There is a lot of pressure for long-term contracts with little sign of movement toward them.

Even worse for the buyers, the EUs exposure to the spot market could hit 50% to meet demand without action.

This is running into problems for other long-term commitments like emission and green energy targets, and politicians are balking.

This is no way to secure lower costs and stem intrinsic inflationary costs, all while demand elsewhere continues to climb. Asia, particularly China, has no qualms with securing long-term contracts.

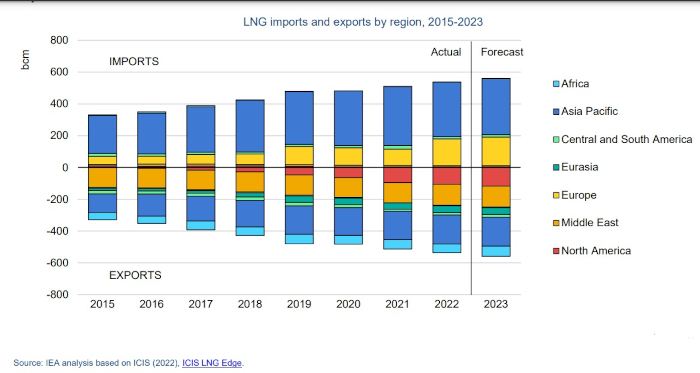

For a global snapshot, here is a chart from the International Energy Agency:

For what it is worth – and it is worth a lot – spot LNG prices have dropped over 82% since the peak in the wake of Russia's invasion of Ukraine.

That isn't how exporters normally want to sell. 25-year terms for major contracts are common. They aren't even allowed by some European laws. Take Germany, for example. Natural gas isn't allowed for green energy targets encoded in passed laws past 2043.

Such a large buying bloc of nations like the EU could flex a bit, but it has been fragmented, to be kind, in its response.

That isn't to say nothing is happening. Germany's only deep water port in Wilhelmshaven is expected to see a 5.5 bill Euro influx of investment to build LNG import capacity. Yet nothing of worth can happen overnight or even over the next couple of years.

With current plans, the investment and capacity increase will pan out through 2030 — a mere 13 years from Germany's self-imposed cut-off date.

How to Profit from Oil and Natural Gas Going Forward

As for how to profit from oil and natural gas, it is all about production, cost, and, ultimately, how profits are returned to investors.

Many commodity companies are saddled with debt that has to be rolled over into higher interest rates. There is no way around that in this economy.

However, many are in an excellent position to continue to return excess profits to shareholders. A particularly useful investing style while the broader stock market is in turmoil.

In years past, that used to be almost exclusively through share repurchasing. That is still happening, and it supports share prices, but it is not what investors want.

Instead, disbursements – primarily high-yield dividends – remain a strong way of securing consistent returns.

I talked about this extensively in the latest issue of our monthly newsletter, which you can sign up for right here.

Of note, a company with a 12% is in a unique position to return a windfall as a buyout target and has the bargaining position to keep paying shareholders while they demand a premium markup to their share price.

It's a rare opportunity. I hope you'll check it out.

Take Care,

Adam English

The Profit Sector