They say all politics is local… and while we might like to mull the state of global geopolitics and talk about what’s wrong with the world and how it might be fixed, we as individuals aren’t likely to ever cast much of a shadow on the big picture.

And so we try to raise our kids right, take good and thoughtful actions in our careers, recycle, keep up with the news, and cut down on red meat. We do what we can and trust that maybe the collective of people acting locally actually ripples outward and makes the world a better place.

Maybe I’m just grumpy. But I think America is awakening to the likelihood that it’s not working quite like we thought and hoped it would.

Plenty of countries have enjoyed higher standards of living by virtue of their willing participation and partnership with what I’ve called “Western economic idealism,” for lack of a better term. And then we have Iran, Russia, Saudi Arabia, China, Afghanistan, Pakistan, etc.

Countries that have made it pretty clear that, frankly, dear readers, they don’t give a damn.

I know I just wrote about this idea last week: that globalization is in retreat, that the world is fracturing along geopolitical fault lines.

But I’m going to keep at it because this trend has huge implications for your investments for the next decade, at least.

We’ve already heard from companies as they pulled out of Russia. Russia and Ukraine combined made up 9% of McDonald’s (NYSE: MCD) total revenue in 2021 – a little over $500 million. Starbucks (NASDAQ: SBUX) had much less Russian exposure, less than 1% of revenue. Still, that’s around $300 million lopped off the top line.

These are not particularly big numbers. But a few hundred million here, a few hundred million there, pretty soon we’re talking about real money…

The Giant Panda in the Room

So let’s go ahead and address the giant panda in the room, China.

In an escalating trade war, what about all the multinational companies that do significant business in China? Companies like Starbucks (NASDAQ: SBUX), General Motors (NYSE: GM), Microsoft (NASDAQ: MSFT), Boeing (NYSE: BA), Apple (NASDAQ: AAPL), Tesla (NASDAQ: TSLA), and so on and so on….

And what about companies that have supply chains that run through China?

How should individual investors proceed as tensions escalate between the U.S. and China? How will this affect the economic and investment landscape?

China’s Trade War

As I wrote last week, simply not owning Chinese stocks that are listed here in the U.S. is a critical step for any investor's financial health. But the potential effects of a growing trade war with China may not be so obvious.

Let’s start with a little history…

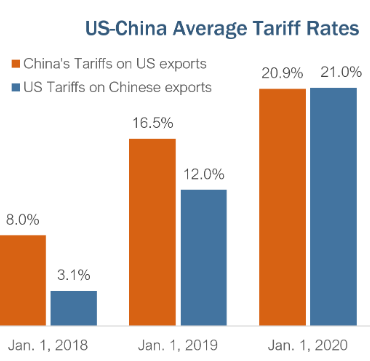

President Clinton paved the way for China to be admitted into the World Trade Organization on January 11, 2001, negotiating a range of criteria on things like intellectual property and human rights to make it happen.

Of course, China ignored or openly violated most of these criteria from the get-go. But the Bush administration had bigger fish to fry with its focus on the War on Terror. In the wake of the financial crisis, the Obama administration began to criticize China and its trade practices openly. But the net result of the tough talk was just complaints filed with the WTO.

President Trump took action in 2018 when he levied a bunch of tariffs on a range of Chinese exports to the US. The dollar value of these tariffs has gone up ever since…

The Biden administration has continued to enforce Trump-era tariffs. It has also added to them. And the most important escalation of this trade war with China concerns the new rules that president Biden enacted for selling semiconductors and semiconductor equipment to China. In a nutshell, selling semiconductors and semiconductor equipment is now illegal. I’ve written about the details of these new rules here.

These new semiconductor and semiconductor equipment rules are less than a month old. China has yet to respond formally, but make no mistake: there will be a response. And I think casino companies operating in Macau are particularly vulnerable.

Wynn Resorts (NASDAQ: WYNN) gets 72% of its revenue from China. Las Vegas Sands is lower, 62%, but both are still largely dependent on China. WYNN was trading at $74 on October 7, the day the Biden semiconductor rules were announced. 5 days later, WYNN shares hit a low of $56.

I’d be wary of pushing all my chips in on the casino stocks like Wynn and Las Vegas Sands. But what about chip stocks?

Chips, Stocks, and China

The sectors of the S&P 500 that get the largest percentage of their annual revenue from China are Consumer Discretionary (companies like Nike (NYSE: NKE) and Tesla), Info Tech (Apple and semiconductors), Industrials, and Healthcare. Each of these sectors gets at least 30% of its revenue from China.

Major semiconductor companies get between 17%-18% Teradyne (NYSE: TER) and Micron (NYSE: MU), respectively) and 45% Nvidia (NASDAQ: NVDA) from China. A few other notable examples: Advanced Micro Devices (NASDAQ: AMD) gets 39% of its revenue from China, Qualcomm (NASDAQ: QCOM) clocks in at 35%, and Wolfspeed (NASDAQ: WOLF) stands at 34%.

These are big numbers, and they are going to go down significantly. I can’t say for sure that chip revenue from China will go to zero because companies can apply for partial exemptions from the Biden semiconductor rules. Still, the main question to ask is how much of this revenue can be offset by non-China sales.

Micron is a good place to begin. It already has manufacturing in the U.S. and is on the low end of the China exposure spectrum. Yes, DRAM and NAND memory are suffering price declines. But memory chip cycles are always volatile. Micron will recover at some point.

The thing to watch as a gauge for the memory chip cycle is Micron’s forward Price-to-Earnings (P/E) ratio.

(Editor’s Note: What’s the P/E ratio? The P/E ratio tells investors how much a company is worth. The P/E ratio is the stock price divided by the company's earnings per share for a designated period, like the past 12 months. The price/earnings ratio conveys how much investors will pay per share for $1 of earnings. The market average P/E ratio currently ranges from 20-25.)

When demand is strong, and prices for memory chips are high, Micron trades with a very low trailing P/E ratio. Right now, that trailing P/E is around 7. Sounds like a bargain, right?

Well, Micron’s forward P/E is 47. This means that analysts expect that Micron will see a dramatic drop in earnings next year. Maybe not such a bargain?

The perception that Micron is a value trap will keep a lot of investors from buying the stock. But the thing is, there are only three major memory chip stocks out there: Samsung and Hynix are in South Korea, and Micron is in the U.S.

When demand and prices fall, these three will cut production to support prices, and they’ll go right back to making boatloads of money when demand returns. So watch that forward P/E ratio. It’s high now and could go higher. But the minute it starts to fall, the stock will rally.

Advanced Micro Devices (NYSE: AMD) has two manufacturing locations in Germany. Taiwan Semiconductor (NYSE: TSM) also makes chips for AMD. The risk for anything Taiwan-related with regard to China is self-evident. But AMD doesn’t have all its eggs in that basket, so that’s a positive. And the progress it’s made in taking market share from Intel (NASDAQ: INTC) for data center chips is also a positive.

Like AMD, Wolfspeed (NASDAQ: WOLF) has high exposure to China. But WOLF is also a special case because it makes silicon carbide chips, which are the go-to for electric vehicle (EV) manufacturing. So, WOLF’s exposure to China is in the EV market. Given the exponentially rising global demand for silicon carbide chips, I think WOLF can easily transition away from China. Wolfspeed shares were recently crushed after earnings.

Last week I told you that buying WOLF shares at $85 was a good idea. This week closer to $80 is even better.

A Word About Supply Chains

I see two promising investment trends forming as companies move supply chains out of China. Mining is one, specifically mining for rare earth and lithium.

The second is 3D printing. As manufacturing moves back to the U.S., it sets the stage for a big surge for various parts, components, and finished products to be 3D printed. And 3D printing stocks are virtually ignored these days, so some very compelling investments exist.

I’m going to dig into these two ideas later this week with a couple of new stocks, so stay tuned…

Until next time,

Brit Ryle

The Profit Sector